Economic Commentary

The second quarter of 2025 kicked off with President Trump’s April 2nd “Liberation Day” announcement of tariffs on nearly every US trading partner. The tariffs were derived from each country’s trade imbalance with the US and were far higher than nearly anyone expected, ranging from 11% to 49%. The unexpectedly aggressive approach sent stocks into correction territory under the assumption that the tariffs would make global recession unavoidable. The panic was short-lived, however, as President Trump issued a ninety day pause just seven days later after various business leaders warned that the tariffs would cause inflation and recession. Trump instead opted for a 10% across-the-board baseline tariff while the administration targeted a goal of “90 deals in 90 days.” China was notably excluded from the pause for retaliating, which commenced a tit-for-tat period of escalation that saw US-China tariffs reaching an almost comical level of 125%, with threats to go higher, effectively eliminating all trade between the two countries.

Cooler heads prevailed in early May with the US and China agreeing to tariffs of 10%. Since then, investors and economists have struggled to get a handle on a whirlwind of on-again, off-again trade war announcements, leaks, and rumors, with the added complexity of the US Court of International Trade (CIT) declaring the tariffs unlawful. The CIT ruling was, of course, appealed by the Trump administration and the tariffs remain in effect while the case works its way through the court system and most likely to the Supreme Court.

The US joined Israel in military action against Iran, which resulted in tariffs to fade a bit as the main driver of markets, but as the quarter ended the cessation of the ninety day pause looms on July 9th, causing many to wonder what’s next. To date, the administration has only signed a single trade deal of limited scope with the United Kingdom, falling far short of the targeted 90 deals.

The effects of the tariffs extend far beyond the simple monetary charges being placed on goods. While not ideal, businesses and economists can adapt to tariffs. The problem with these tariffs has been the completely unpredictable and constantly changing nature of the announcements. 91% of S&P 500 companies cited tariff uncertainty in first-quarter earnings calls, with some companies withdrawing earnings guidance due to the unknown and rapidly shifting nature of the tariff war.

The US Federal Reserve (“the Fed”) has been similarly paralyzed by tariff uncertainty. At the start of the year, it was widely anticipated that the Fed would take a first-quarter breather on rate cuts to assess the impact of President Trump’s trade policy. Now halfway through the year, the Fed has not gained enough clarity to resume rate cuts. During recent Congressional testimony, Chairman Jerome Powell suggested that, absent the tariffs, the Fed would have already cut rates. As it stands, the Fed is hesitant to cut with most economists agreeing that the net effect of tariffs is higher domestic inflation and reduced economic output, the dreaded “stagflation” scenario that the Fed has less power to combat.

Powell also noted the Fed is placing more weight on forward-looking inflation projections than the trailing inflation data, which has been relatively benign at an annual rate of 2.7% (using the Fed’s official measure of the Core Personal Consumption Expenditures Index, or “PCE”). The Fed is projecting Core PCE will rise to 3.1% by the end of the year as tariff costs work their way through the economy. Despite this expected uptick in inflation, the Fed has been quick to point out that the US economy is otherwise on very strong footing with solid wage growth, low unemployment, and healthy consumer spending that should keep the US out of a recession despite a diminished 2025 GDP growth rate forecast of 1.4%.

Market Commentary

US stocks sold off in unison on the “Liberation Day” tariff reveal but quickly regained the lost ground. The S&P 500 was up an impressive 10.9% during the quarter. Yet, the “everything rally” of late 2024-early 2025 has faded and the second quarter saw more bifurcated performance in US equities with clear winners and losers. Technology sector stocks (using the SPDR Technology Sector ETF, XLK) returned to a leadership role with an impressive 22.8% quarterly return, including a 41.1% bounce off the April 8th low. Impressive earnings from mega-cap technology stocks and continued optimism for anything with exposure to artificial intelligence (AI) were the main themes of the earnings season, aside from tariffs of course. Earnings calls showed a continued commitment to heavy spending on AI across all industries. Despite Middle East turmoil that caused a temporary spike in oil prices, Energy sector stocks (represented by the SPDR Energy Sector ETF, XLE) were the biggest laggard during the quarter, losing 8.5% due to stagflation concerns, a continued long-term downward trend on demand, and a global oversupply of oil. After all that volatility, however, thankfully US large cap stocks, as represented by the S&P 500 Index, closed the quarter very near all-time highs. Just keep your seat belt buckled.

Small and mid-cap US equities are typically considered to be more resilient to trade war dynamics, since they often operate more domestically than large-cap multinationals. Yet small and mid-caps underperformed during the second quarter due to their relative inability to absorb input cost increases compared to their larger peers. The cost of tariffs is borne by the importer, and while large companies have expressed a willingness to at least temporarily eat some of those costs, smaller companies often lack that luxury. Smaller companies have also been desperately awaiting rate cuts to facilitate financing of capital expenditures, and to refinance maturing debt, but as mentioned the tariffs have prolonged the Fed’s wait-and-see posture, keeping rates higher than liked.

While the tariffs were meant to be punitive for the rest of the world, Developed and Emerging Market (EM) stocks kept pace with their US counterparts in the second quarter. The MSCI EAFE index gained 11.3% while the MSCI Emerging Market index outperformed with a 11.4% quarterly return. China responded to US trade threats with both reciprocal tariffs and policy measures to spur domestic investment and infrastructure improvements. Emerging markets also benefitted from a weaker US dollar, which partially offset the tariff impact on goods exported to the US.

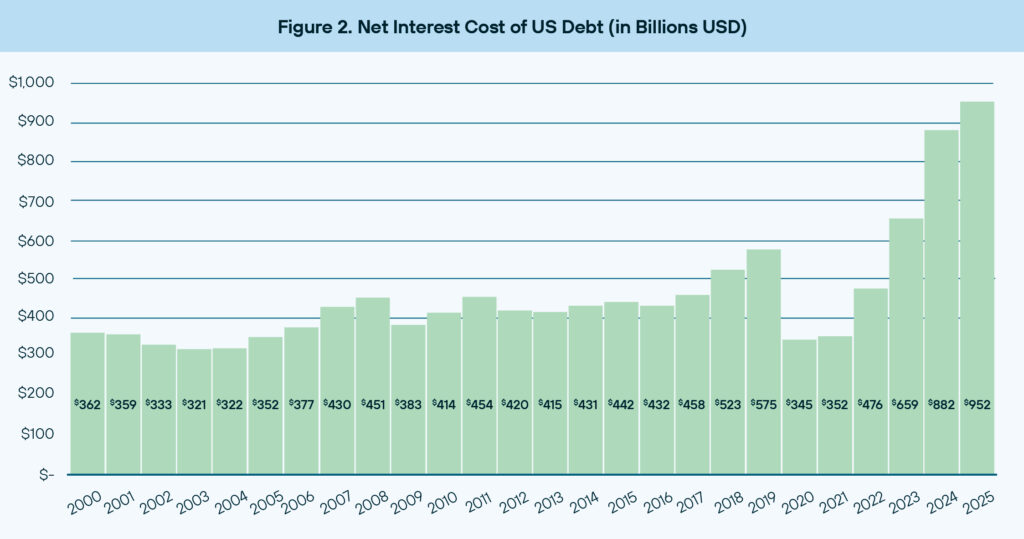

Foreign stocks and bonds also had the tailwind of rate cuts in their markets, which lowered borrowing costs, bolstering investment and growth. The European Central Bank has cut rates eight times this cycle, bringing its benchmark borrowing rate down from 4.5% to 2.15%. Meanwhile, the US Federal Funds rate remains at 4.25%-4.5%. While the Fed’s decision to keep interest rates elevated affords them some “dry powder” in the event of a recession, it is also costing US taxpayers nearly a trillion dollars in annual interest payments on the ever-growing Federal debt.

For fixed income investors, US government bonds failed to deliver during the brief, but quite notable moment this past quarter of “risk-off” due to tariff driven recession concerns. 10-Year US Treasury yields rose from 4% to 4.5% during the initial tariff shock in early April as investors sold both stocks and bonds. Even after the ninety-day pause was initiated, Treasury yields remained elevated. Concerns over the GOP tax bill, which is expected to add $3 trillion to the deficit over the next decade, have soured investors on US government debt and prompted Moody’s to downgrade the US credit rating from AAA to Aa1.

Foreign investors have also taken note, with speculation that Japan and other holders of US bonds are increasingly looking to diversify away from US debt, and the US Dollar.

While fixed income investors shied away from government bonds during the quarter, corporate bond demand remained solid, with investment grade and high yield bonds both benefiting from continued solid issuance. High yield bond spreads were relatively unchanged during the quarter, down slightly to 3.1%, which remains well below the long-term average of 5.3% and is not indicative of any recession worries.

Closing Remarks

Prior to the announcement of tariffs, we noted that the impact could be fleeting if trade deals were quickly struck. Trade deals have yet to materialize, but the tariff shock has faded, and markets have begun to factor in President Trump’s tendency to walk back his more incendiary policies when they cause adverse economic effects. It is likely that the ninety-day respite will not end with significant trade deals, but the tariffs may be lowered regardless. This would give the Fed an opportunity to get a September rate cut in and provide markets with an upside catalyst. Uncertainty has not dissipated, but the trade war remains a self-inflicted wound that can quickly heal.

Thank you for the opportunity to be of service.