WEEKLY MARKET SUMMARY

Global Equities: Stocks navigated another week of geopolitical turmoil, with early-week escalation giving way to progress on a “Memorandum of Understanding” in the latter half of the week. Tech stocks continued to lead the way, with software stocks showing relative strength as worries over the impact of AI faded on good earnings news. The S&P 500 and Nasdaq Composite hit new record highs, gaining 1.4% and 2.4%, respectively. The Dow Jones Industrial Average was also higher on the week, gaining 0.9%, while US small caps rose 1.9%. Foreign Developed stocks were up modestly on the prospects of energy relief from an Iran deal, gaining 0.8% during the week. Emerging markets were the biggest gainers thanks to a surge in Korean and Taiwanese semiconductor stocks, soaring 4.1% in the weekly period.

Fixed Income: Treasury yields eased in the latter half of the week, shrugging off hot inflation data on geopolitical optimism. The 10-year Treasury note yield eased to around 4.44% on Friday, its lowest level in more than two weeks. Markets currently expect the Fed to keep the federal funds rate unchanged through year-end, though investors still assign roughly a 46% probability to a rate hike in December.

Commodities: WTI crude oil futures fell approximately 2% to around $87 per barrel on Friday, their lowest level in roughly six weeks, putting them on track for a roughly 17% decline in May. Technical analysts noted that WTI appears to have completed a head-and-shoulders pattern on the daily chart, with the head peaking near $108 per barrel in April, suggesting the recent geopolitical risk premium has begun to unwind materially. Gold prices edged higher, with spot gold trading near $4,530 per ounce on Friday.

WEEKLY ECONOMIC SUMMARY

April PCE Inflation: The Fed’s preferred inflation gauge, the Personal Consumption Expenditure (PCE) Index, delivered a mixed message on Thursday. The Iran war’s oil price shock lifted the headline PCE inflation rate to a three-year high of 3.8% in April on a year-over-year basis. Core PCE, which excludes food and energy, rose 0.2% for the month, a deceleration from 0.3% in March, though the annual rate ticked up to 3.3%. The headline number will likely exceed 4% in the May PCE report, which will be released June 25th.

Iran War Update: US and Iranian negotiators reached an agreement on a 60-day memorandum of understanding to extend the ceasefire and launch negotiations on Iran’s nuclear program, though President Trump had not yet given his final approval and Iran had also not confirmed its acceptance. Under the proposed framework, the Strait of Hormuz would reopen with no tolls during the 60-day period, Iran would be permitted to freely sell oil, and negotiations would be held on curbing Iran’s nuclear activities. Reportedly, Iran would also receive a $300 billion “investment fund”, which could satisfy the regime’s demand of compensation for damages incurred during the conflict.

Earnings Season: Dell Technologies (DELL) stepped into the earnings spotlight and delivered an unexpectedly strong report. Revenue climbed 88% year over year to $43.8 billion, crushing estimates by roughly $9 billion, while adjusted EPS jumped 214% to $4.86. Software stocks got a boost from a strong earnings beat from Snowflake (SNOW), sending shares of the cloud data platform over 36% higher.

The week ahead: The tail end of first-quarter earnings reports trickle in, with Broadcom (AVGO) and Crowdstrike (CRWD) results slated for midweek. Economic data highlights include the Institute for Supply Management reports on Manufacturing and Services, the Fed’s Beige Book, and the May Jobs report.

CHART OF THE WEEK

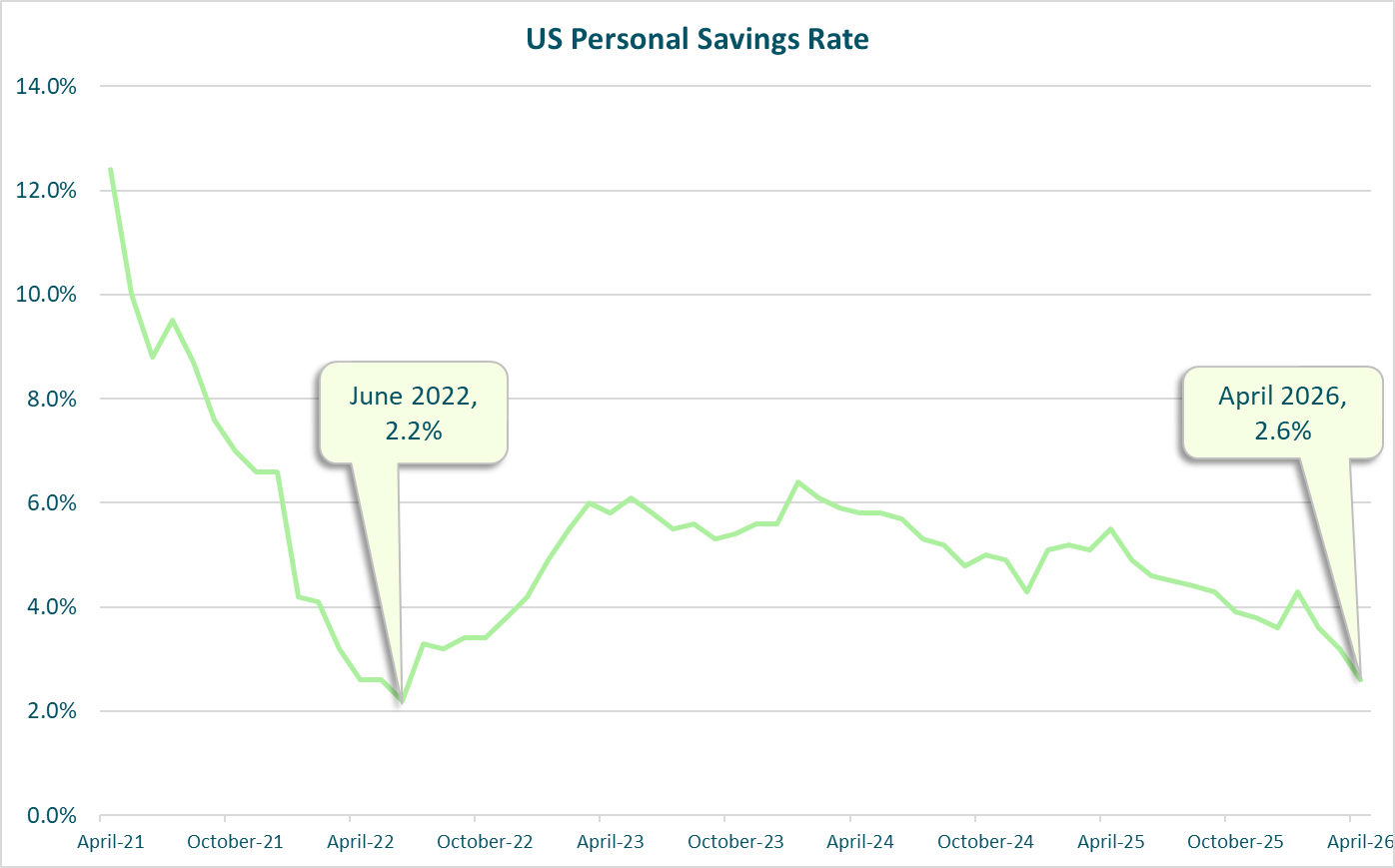

The Chart of the Week examines the US personal savings rate, which fell to its lowest level since June 2022 in April at 2.6%. For the first time since 2023, consumer price inflation is outpacing wage growth, reducing disposable income. The high cost of essentials, particularly food and gasoline, have whittled away Americans’ financial buffers. While many US taxpayers received increased tax refunds this year, survey data suggests roughly 71% of taxpayers have entirely spent that money. Meanwhile, credit card delinquencies have spiked to a 15-year high and total outstanding credit card debt reached $1.25 trillion in the first quarter, a 5.9% increase over the prior year. A resolution to the Iran conflict would provide a substantial boost to consumer optimism and some relief to household balance sheets.

Chart and commentary by VestGen.