WEEKLY MARKET SUMMARY

Global Equities: Stocks surged during the week, propelled by tech earnings and mid-week optimism over potential peace negotiations between the United States and Iran. The S&P 500 gained 2.4% and the Nasdaq Composite climbed 4.5% on the week, with both indexes closing at fresh all-time highs on Friday and marking their sixth consecutive winning week, the longest streak since 2024. The Dow Jones Industrial Average lagged notably, registering a weekly gain of just 0.3% and falling short of recapturing the 50,000 mark. Small caps gained 1.8% during the week while foreign developed market stocks were up 1.8%. Emerging market stocks outperformed with a 5.9% weekly gain, driven by semiconductor stocks, geopolitical optimism, and a softening US dollar.

Fixed Income: Treasury yields moved higher early in the week, with the 10-year US Treasury note reaching 4.45% as the US and Iran clashed in the Strait of Hormuz but ultimately ended relatively unchanged at 4.36% on Friday as optimism for a potential resolution grew. Better-than-expected jobs data gave Fed hawks further rationale to keep rate cuts on hold, and possibly to argue for hikes. The odds are presently even at 10% for a cut or a hike at the December meeting, with an 80% likelihood that rates end the year unchanged from present levels.

Commodities: Oil prices fell sharply after the US submitted a one-page peace deal to Iran before rebounding but still ended the week lower with West Texas Intermediate around $95 a barrel and Brent Crude around $100 on Friday. The IEA warned that the conflict is disrupting roughly 14 million barrels per day of global oil supply and that any post-conflict production recovery would likely proceed gradually, given insurers’ reluctance to cover tankers crossing the Strait.

WEEKLY ECONOMIC SUMMARY

Consumer Sentiment Sours: The University of Michigan Consumer Sentiment Index dropped to 48.2 in May, down from 49.8 in April and reaching an all-time low. The current reading is significantly lower than levels seen during the 2008 financial crisis or the Covid-19 pandemic, reflecting widespread pessimism from consumers over numerous issues. Energy costs were the primary concern for roughly one-third of respondents as gasoline prices have reached a national average of $4.55/gallon. Concerns over high prices for groceries and goods, and the impact of tariffs also registered as major areas of concern. Inflation expectations for the coming year remain elevated at 4.5%.

April Jobs Data: The April Employment Situation report showed nonfarm payroll gains of 115,000, easily surpassing estimates of 63,000 as the unemployment rate remained unchanged at 4.3%. While the headline numbers look strong, there was some cause for concern in the underlying data, particularly due to the narrow breadth of the job gains with nearly half coming from the Healthcare and Social Assistance sector. The Information Technology sector lost 13,000 jobs, Financial jobs fell by 11,000, and Manufacturing lost 2,000 jobs. Federal jobs also fell by 9,000, bringing Federal employment down 11.5% from the October 2024 peak. Labor force participation also slipped to 61.8%, the lowest level since October 2021, as 92,000 people dropped out of the work force. The number of workers taking on part-time work for economic reasons surged by 445,000, reaching a total of 4.9 million.

Earnings Season: Semiconductor stock earnings have reignited the AI trade, with insatiable demand for computing power driving record results. AMD (AMD) posted 57% growth in AI datacenter business, propelling shares 18% higher after results. Shares of Super Micro Computer (SMCI) also soared post-earnings, up 13% after revenue more than doubled.

The week ahead: Consumer Price Index inflation data is due out May 12th and Producer Price data follows on May 13th. Alibaba (BABA) and Cisco (CSCO) highlight a relatively light week for major earnings news, with Nvidia (NVDA) earnings not due out until May 20th.

CHART OF THE WEEK

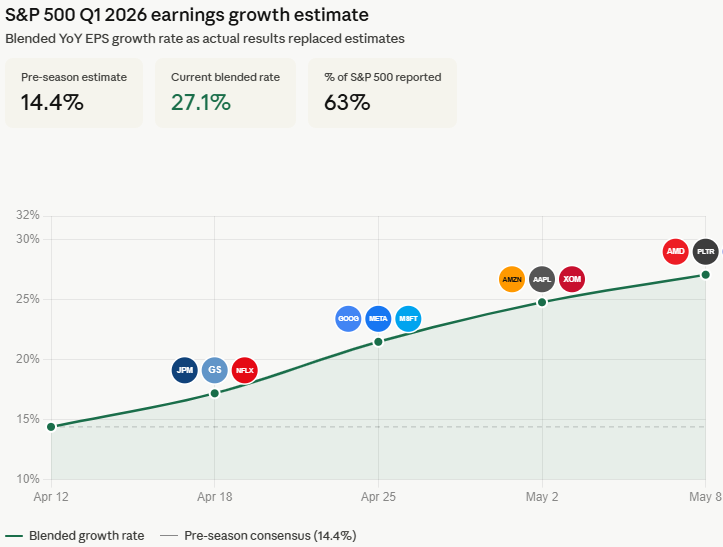

The Chart of the Week shows the upward revision to S&P 500 earnings growth for the first quarter, with roughly two-thirds of companies done reporting. The blended EPS growth rate, which combines actual reported earnings with estimates for companies yet to report, is tracking at 27.1% year-over-year, nearly double initial estimates. The single biggest jump occurred during the April week of Mag 7 earnings, which tacked on 4.3% to the earnings growth rate. Companies have also missed estimates at the lowest rate in 25 years. With one-third of the S&P 500 yet to report, the final rate could possibly clear 30%, which would rank among the strongest earnings seasons since the post-Covid recovery in 2021.