WEEKLY MARKET SUMMARY

Global Equities: Rising Treasury yields began to weigh on stocks in the first half of the week, but those concerns faded as the long weekend approached with fresh optimism for a potential Iran peace deal. The S&P 500 ended the week 0.9% higher and the Dow Jones Industrial Average gained 2.1% to close at a new record high of 50,580. The Nasdaq Composite was a relative laggard at 0.5% as investors rotated out of technology names and into other neglected sectors of the market. Small cap stocks slipped early in the week on interest rate concerns but recovered to gain 2.7%. Foreign Developed Market stocks ended the week up 2.2%, while Emerging Markets closed 1.2% higher on the prospect of an Iranian peace deal.

Fixed Income: The increasing likelihood of a possible Fed rate hike began to weigh on Treasury yields. The 10-Year note hit its highest level in over a year at 4.67%, although yields eased to end the week at 4.58%. The 30-Year yield also reached its highest point in over a year at 5.2% before pulling back to 5.08%. Minutes from Jerome Powell’s final Fed meeting revealed a majority of Fed officials in favor of rate increases if the Iran war continued to impact inflation. Odds of a rate hike before year-end ended the week at roughly 70%, with no chance of a cut being priced in.

Commodities: The ever-shifting narrative surrounding possible peace in Iran caused oil prices to whipsaw wildly during the week. US benchmark West Texas Intermediate (WTI) began the week at nearly $110 a barrel but retreated to the mid-$90s after a fresh proposal for ending the Iran war surfaced. Gold prices have remained relatively flat since late March, ending the week relatively unchanged at $4,515/oz.

WEEKLY ECONOMIC SUMMARY

Consumer Sentiment Sets New Low: The University of Michigan Consumer Sentiment survey plummeted to the lowest-ever reading in the 74-year history of the index, at 44.8 in the final May 2026 report. High gas prices have consumers feeling dismal on the prospects for the US economy and their household budgets. 57% of respondents reported high prices are eroding their personal finances, with low-income households reporting the most pessimism. Respondents also don’t anticipate any near-term improvement in inflation, with the one-year expectation at 4.8% and long-run inflation expectations at 3.9%.

Iran War Update: The week began with heated rhetoric from President Trump with Sunday threats that “the clock is ticking” for Tehran to accept a deal, threatening there “won’t be anything left of them” if Iran didn’t accept US terms. The mood shifted towards optimism by Tuesday after Trump stated he paused a scheduled military attack at the behest of the Qatari, Saudi, and UAE leaders. Trump characterized “serious negotiations” as positive, although Iranian stated media called the US pause a “retreat”. Reports that both sides are getting closer gave markets some reason for optimism heading into the long weekend, but US Secretary of State Marco Rubio cautioned that the US would maintain a “Plan B” if negotiations collapse.

Earnings Season: Nvidia (NVDA) hit the earnings stage mid-week, delivering another staggering quarter of results. Quarterly revenue of $81.6 billion beat estimates of $78.8 billion and $1.87 EPS exceeded the forecasted $1.76. Data center revenue grew at 92% year-over-year. Nvidia also allocated an additional $80 billion to share repurchases and raised the dividend to 25 cents per share. Despite the jaw-dropping results, shares moved lower post-earnings, as has been the trend in recent quarters for the world’s most valuable company.

The week ahead: A holiday-shortened week kicks off with fresh data on Consumer Confidence from the Conference Board on Tuesday. Investors will also get the first estimate of Q1 GDP on Thursday, along with the Fed’s preferred inflation indicator, the Personal Consumption Expenditures (PCE) Index.

CHART OF THE WEEK

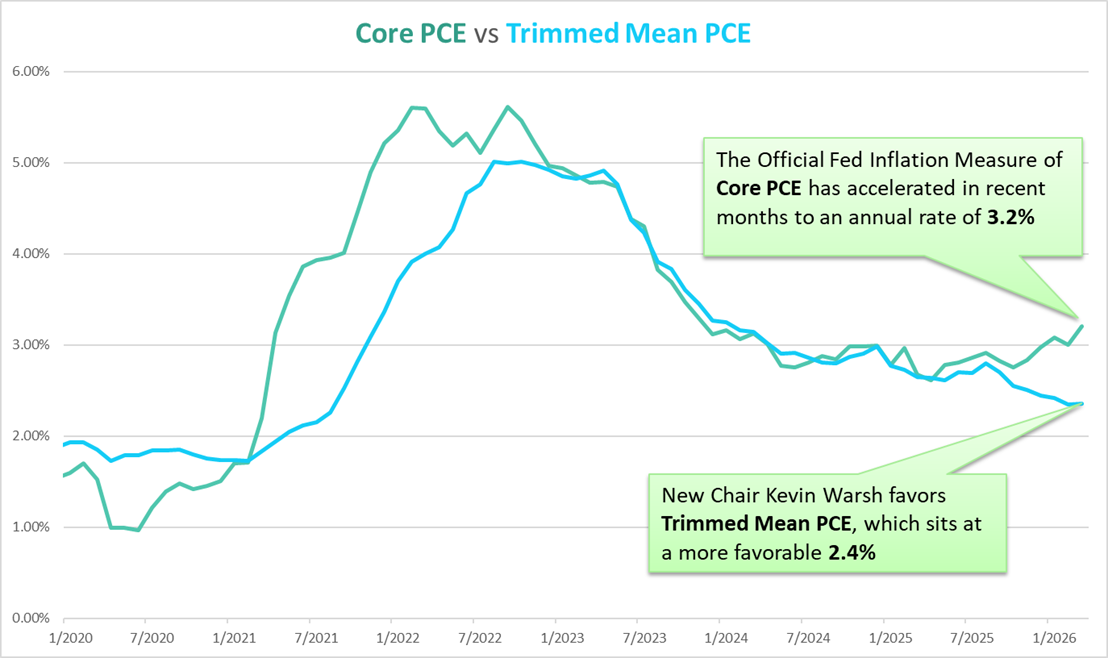

The Chart of the Week looks at an alternative measure of inflation data that could possibly be in the headlines as new Chair Kevin Warsh takes the helm at the Federal Reserve. In his swearing-in speech, Warsh highlighted his desire to reform outdated economic data models, reduce contradictory “Fedspeak” from regional Fed presidents, and eventually unwind the Fed balance sheet.

One change that Warsh may seek to implement is a revision of the Fed’s official inflation measure from Core PCE to a little-known alternative measure, Trimmed Mean PCE. Core PCE removes food and energy from inflation calculations since these two categories are historically most prone to month-to-month volatility. Trimmed Mean PCE uses a more dynamic approach, filtering out the most volatile price changes at both the high and low ends on any given month. The categories removed can vary month to month, resulting in a smoother picture of inflation as shown in the blue line on the chart. Critics of Trimmed Mean PCE caution that large price swings are not always “noise”, and the filtering method can underestimate broad, sustained price increases.

Warsh publicly mentioned his preference for Trimmed Mean PCE during his Senate confirmation hearing. If he can successfully lobby for a change in the inflation benchmark, the Trimmed Mean PCE rate of 2.4% inflation would put the Fed much closer to its target 2% inflation goal than the current 3.2% Core PCE reading, providing Fed doves with rationale for rate cuts.

Chart and commentary by VestGen.