WEEKLY MARKET SUMMARY

Global Equities: Stocks continued to sell off as investors grew skeptical of a diplomatic resolution to the conflict in Iran. A five-day pause in US strikes against energy infrastructure prompted an early-week rally, but those hopes faded as the reprieve expired at the end of the week, despite the announcement of a ten-day extension early Friday. The S&P 500 ended the weekly session down -2.1% and on the verge of joining the Nasdaq Composite and Dow Jones Industrial Average in technical correction territory. The Nasdaq ended the week -3.2% lower, while the Dow slipped -0.9%. US small caps fared relatively better despite being more sensitive to rising interest rates, ending 0.4% higher. Foreign developed market stocks gained 0.2% despite heavy uncertainty over the energy supply for European markets, while emerging markets fell -0.8%.

Fixed Income: Treasury yields continued to grind higher, closing out the week with a 4.44% yield on the 10-year note. Demand was soft across the curve at auctions held during the week, particularly on $69 billion of 2-year notes with primary dealers (bidders of last resort) forced to take 24% of the issuance. Rising yields put further pressure on the housing market, driving the average 30-year fixed rate mortgage to 6.5% and contributing to a -10% decline in weekly mortgage applications. Private credit markets remained as two more firms, Apollo Global Management and Ares Management, capped redemptions.

Commodities: Oil markets whipsawed sharply throughout the week. Prices dropped more than -10% early in the week after President Trump described productive discussions and announced a five-day pause in strikes, raising expectations for a diplomatic resolution. Those gains reversed when Iran denied active negotiations and rejected a formal US ceasefire proposal that included reopening the Strait of Hormuz, which remains closed. Brent crude climbed back above $110 per barrel on Friday as the diplomatic window narrowed, with WTI ending the week at $99. Gold prices were relatively flat during the week, hovering around the $4,500 level.

WEEKLY ECONOMIC SUMMARY

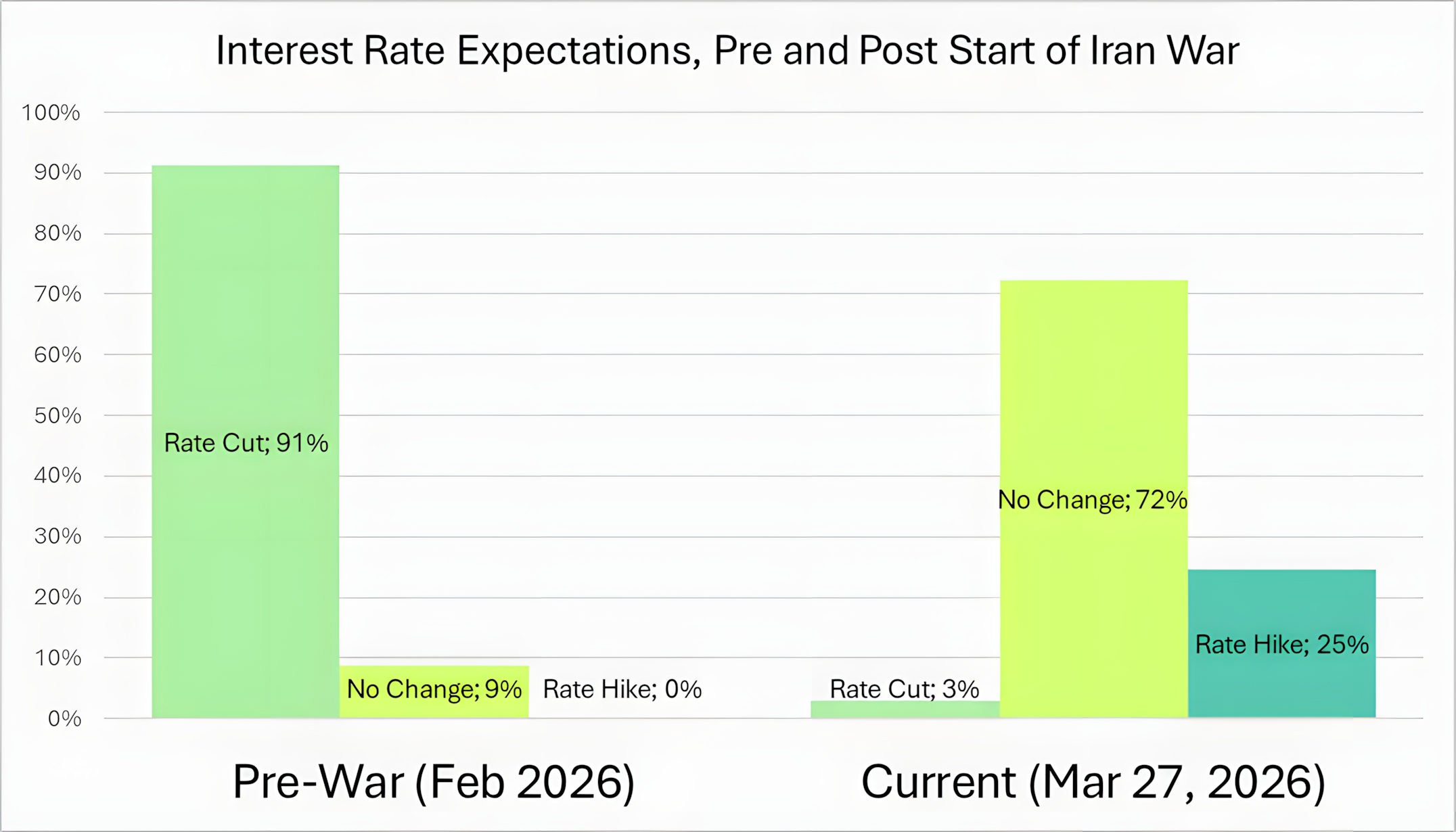

Fed Cuts No Longer Expected: Expectations for a 2026 Fed rate cut have suddenly vanished, with Fed funds futures showing a less-than-5% likelihood of a cut at the Fed’s final meeting of the year in December. The possibility of an energy crisis triggering a recession now has investors pricing in 24% probability for rate hikes by year-end. While President Trump is hoping his pending Fed Chair appointee Kevin Warsh will be an ally at the central bank, he will have a tough time convincing his Fed peers to cut rates as oil prices are poised to drive inflation higher in the coming months.

Consumer Confidence Fades: The University of Michigan’s final March consumer sentiment reading, released Friday, underscored the psychological damage inflicted by the Iran conflict. The sentiment index fell to 53.3, its lowest level since December 2025, as survey data showed a broad-based decline in outlook across all age and demographic groups. High-income households, which have been holding the economy up during the “K-shaped” recovery, showed the sharpest decline in confidence. Inflation remains a major concern, with respondents anticipating a 3.8% rate of inflation for the year.

Housing Market Stress: Rising mortgage rates have created an imbalance of home sellers to buyers, with a record mismatch of 630,000 more sellers than buyers according to a Fortune report. However, the excess supply has yet to translate to downward pressure on home prices, with the median existing home price up 0.3% year-over-year in February to $398,000. Permits for new homes fell -5.4% in January to an annualized rate of 1.366 million, which is the lowest number since August 2025.

CHART OF THE WEEK

The Chart of the Week shows the stark contrast in year-end Fed Funds rate expectations before and after the onset of the war in Iran according to data from CME Group, which tracks daily changes in Fed Funds futures expectations. Prior to the hostilities, markets were betting on when, not if, rate cuts would occur in 2026, with zero implied probability of a rate hike. Initial hopes for a brief conflict are beginning to fade, and the continued closure of the Strait of Hormuz will likely spark higher global inflation. The realization that energy prices may be higher for longer has led markets to all but dismiss any chance of lower interest rates in 2026 as the odds of a cut have fallen from 91% to just 3%, with the possibility of rate hikes now also being priced into markets.

Commentary by VestGen Investment Management.