ECONOMIC COMMENTARY

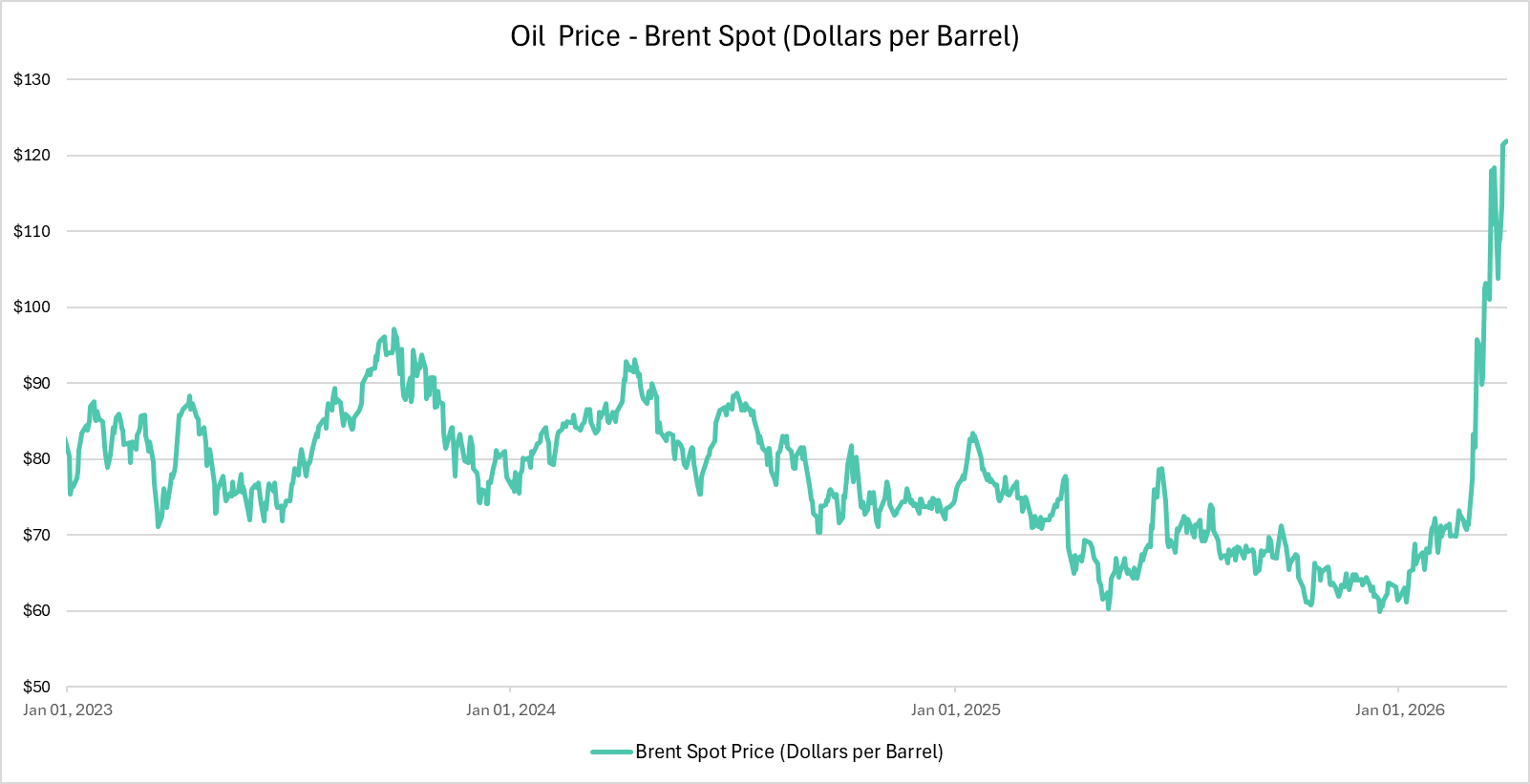

Two months of relative calm were upended by a turbulent March that began when the United States and Israel launched joint air strikes on Iran on February 28th. The sudden conflict, which was preceded by a much more limited military operation in Venezuela, sent shockwaves through global energy markets. Crude oil prices surged as Iran shut down oil tanker traffic through the Strait of Hormuz, triggering concerns over global growth as the conflict remains unresolved at quarter end. Twenty percent of the global daily oil consumption travels through the Strait, although recent reports say about half of that has been diverted to alternate routes.

The geopolitical turmoil triggered a complete repricing of Federal Reserve interest rate policy forecasts. Prior to the Iran conflict, markets were pricing in roughly 91% odds of an interest rate cut before year-end. At quarter end, the probability of a 2026 rate cut stands at around 25%. The Fed held the federal funds target rate steady at 3.50%–3.75% for the second consecutive meeting at its March Federal Open Market Committee (FOMC) gathering, having paused after three consecutive 25-basis-point cuts in September, October, and December of 2025. In its closely watched “dot plot,” the median projection still called for a single rate cut in 2026 with seven participants now penciling in no cuts, up from six. Fed Chairman Jerome Powell acknowledged at his post-meeting press conference that the implications of the Iran conflict remain highly uncertain, and that monetary policy is currently “well positioned” to maintain a wait-and-see approach.

While President Trump has vocally advocated for rate cuts, the Fed is likely to remain hamstrung by the “stagflation” threat of slowing economic growth and rising prices. On the inflation front, the Consumer Price Index (CPI) rose 2.4% year-over-year through February, unchanged from January, while core CPI held at 2.5%. Goods inflation has remained persistently elevated, with the Fed and Chair Powell pointing to ongoing tariff pass-through as a key driver. The energy sector’s impact on headline inflation will accelerate significantly in the months ahead as the oil price surge filters through to gasoline, utilities, and transportation costs.

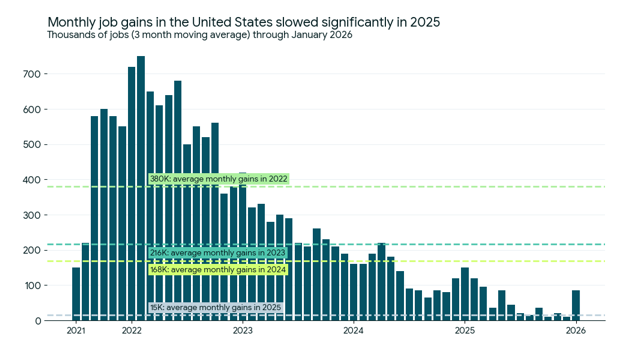

The U.S. labor market continued to reflect a “low-hire, low-fire” dynamic throughout the quarter. The unemployment rate edged back up to 4.4%, approaching the four-year high of 4.5% reached in November 2025. Nonfarm payrolls fell by 92,000 in February, well below expectations of a 59,000 gain. The result was compounded by downward revisions to prior months, including a revision to December that flipped the prior 48,000 job gains to a loss of 17,000, bringing average monthly gains for 2025 down to just 15,000.

Economic growth stalled in the fourth quarter of 2025, decelerating to just 1.4% following Q3’s robust 4.3% GDP print. Looking ahead, the FOMC’s upgraded 2.4% growth forecast for 2026 reflects expectations that the full-year economic tailwind from the One Big Beautiful Bill Act’s tax provisions will more than offset near-term headwinds from the energy shock and labor market softness.

The Fed will once again be in “wait-and-see” mode to begin the new year, despite intense political pressure from President Trump and the likely announcement of a loyalist Fed Chair who will advocate for the President’s demand of much lower rates. Fed policymakers have penciled in only one additional 0.25% rate cut for 2026, while markets anticipate two or three cuts. The voting members of the Fed rotate each year and four mostly-hawkish outgoing members will be replaced by a balanced mix of hawks and doves, skewing the overall committee more dovish, i.e., in favor of rate cuts.

MARKET COMMENTARY

The long-anticipated broadening of market leadership finally materialized in Q1, though the quarter’s overall direction was still negative with the S&P 500 falling 4.6% during the quarter. After carrying the S&P 500 to double-digit calendar year gains in 2023, 2024 and 2025, the “Magnificent Seven” technology stocks fell 13% in the first quarter as investors grew increasingly impatient with massive AI infrastructure spending that had yet to produce proportionate returns on investment. Economic sectors like Energy, Materials, Utilities, and Industrials were the beneficiaries as investors took profits on big Tech shares and diversified into less exciting, but cheaper, defensive sectors. While the rotation into Energy stocks began before the outbreak of war, the oil crunch accelerated the move, leading to a gain of nearly 38% for the sector, which was by far the best performer during the quarter.

Small cap stocks also showed relative strength during the quarter, which may seem counterintuitive given their higher sensitivity to rising interest rates. The Russell 2000 gained nearly 10% during January and was able to maintain those gains until the Iran war triggered a selloff and the index ended the quarter with a slight gain of 0.9%. The structural case for small cap outperformance of attractive valuations, improving earnings growth, and a more favorable regulatory environment remains intact as the second quarter begins.

Proponents of the benefits of a diversified global portfolio were vindicated by relative strength in foreign Developed Market (DM) stocks, which benefited from US dollar weakness, more favorable inflation trajectories, and government stimulus measures. The MSCI EAFE index built on its remarkable 32% 2025 return, posting a strong positive result through the first two months of the quarter before giving back some gains as the Iran conflict weighed on global risk appetite in March. EAFE was able to finish the quarter positive at 1.2%. Japan was a notable bright spot to start the year, with the Nikkei 225 surging over 10% in February alone as new Prime Minister Takaichi’s pro-growth agenda continued to attract global capital. March, however, saw the Nikkei suffer its worst monthly decline since 2008 as oil prices and geopolitical uncertainty triggered a broad risk-off selloff across global markets.

The backdrop for Emerging Market (EM) equities was more challenging as the energy shock proved more disruptive to their inflation and current account dynamics. While a weaker US dollar remained a supportive tailwind, the sharp rise in energy import costs weighed on EM economies that rely heavily on Middle Eastern supply. Despite these structural challenges, EM stocks outperformed both US and DM stocks in the quarter with a 3.8% gain.

Fixed income markets faced significant headwinds in the latter half of the quarter as the Iran conflict rekindled inflation fears and caused investors to price out the prospect of Fed rate cuts. The 10-year Treasury yield, which had traded in a range of 4.0%–4.25% for much of January and February, surged to 4.36% by quarter-end, as inflation worries and concerns over persistent deficit spending pushed the risk premium higher. The Bloomberg U.S. Aggregate Bond Index posted a slim positive return in January before giving back gains as yields rose in March, ending the quarter flat on a total return basis. Bonds failed to provide “risk-off” diversification benefits as stocks and bonds fell in tandem for much of March.

Short-duration assets and investment-grade credit fared better than long Treasuries, as the Fed’s pause anchored the front end of the yield curve. High yield corporate bonds had a constructive start to the year given tight credit spreads and solid earnings. High yield sold off along with equities as recession odds increased due to the war and energy crunch, ending the quarter down -0.8%. Despite the negative quarter, high yield bond indices were mostly insulated from private credit concerns that dominated headlines, due to their low underlying Technology credit exposure and higher exposure to Energy sector bonds.

Commodities were extremely volatile during the quarter, highlighted by a surge in oil prices that saw Brent crude prices rising as high as $117 per barrel after starting the year at just under $61. While Iran is vastly overpowered in the fight against the combined military might of the US and Israel, it holds a strategic geographic advantage over the Strait of Hormuz. Iran attacked several tankers in the strait, and the continued threat of hostilities has forced oil tankers to either stop traveling through the waterway or pay a toll of up to $2 million per ship to the Iranian regime for safe passage. While President Trump has recently stated he is willing to walk away without retaking the Strait of Hormuz, a resolution is desperately needed to prevent global energy prices from rising even higher. Outside of oil, other commodities also swung wildly during the quarter, highlighted by gold prices, which surged to a record peak of $5,595/oz on January 28th before falling as low as $4,100/oz in late March. Gold ended the quarter at roughly $4,500/oz.

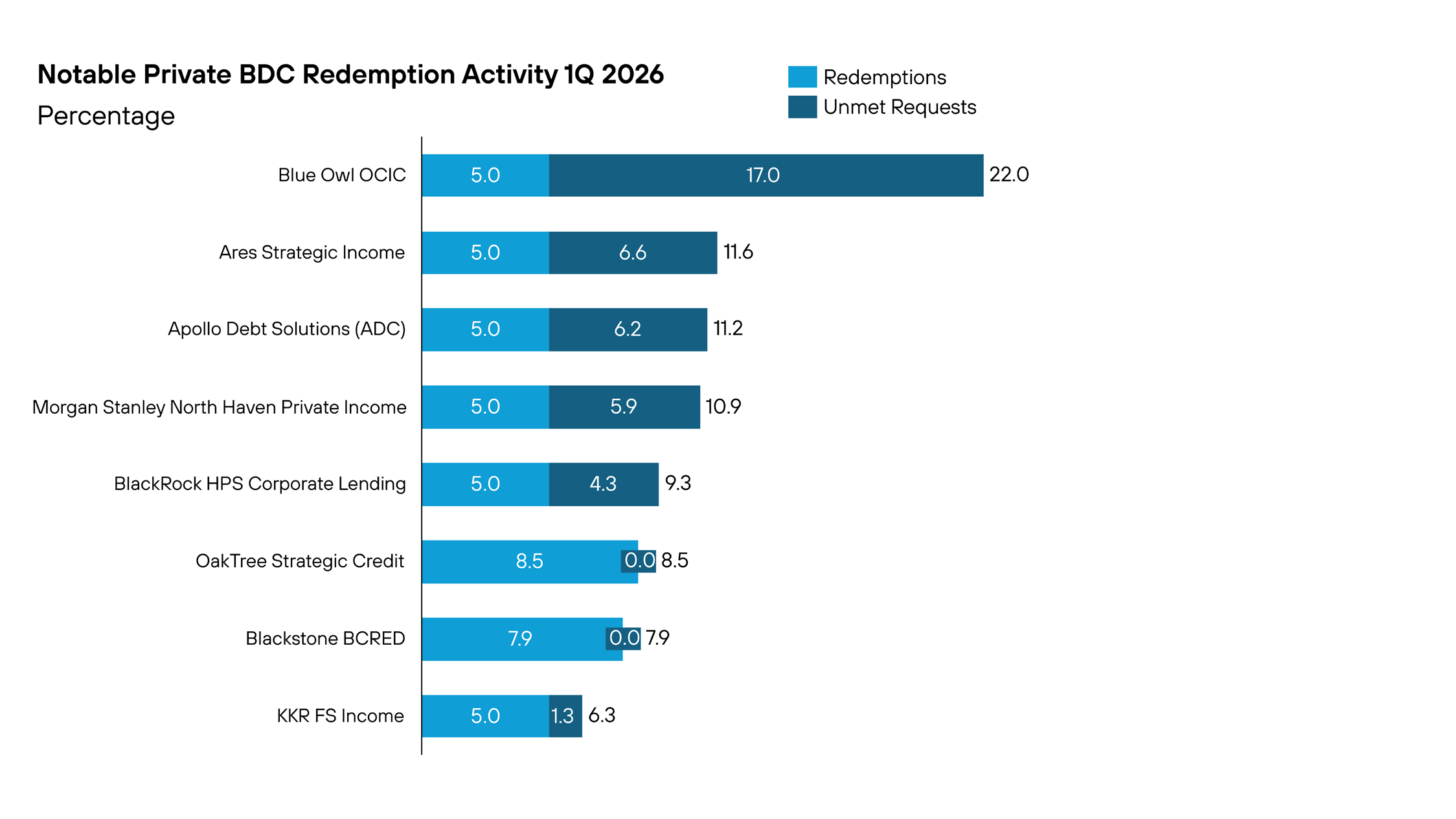

In the area of alternative investments, Private Credit made a number of headlines as semi-liquid, privately traded business development corporations (BDCs) faced larger than typical redemption requests. A confluence of factors contributed to these redemptions including fears about heavy exposure to technology companies subject to disruption from AI and concerns about stale pricing policies for fund valuation. As a result, most of these flagship funds did not satisfy all the demand for fund redemptions in 1Q.

While demand for liquidity does not appear to be spreading to other asset classes at this time, it is an interesting situation to monitor and is expected to continue for several quarters as investors seeking liquidity will add to their future redemption requests, expecting to only get a portion of their assets back. Should investor concern spread, it might result in a broader economic deleveraging.

Investors who looked beyond the borders of the US were rewarded in 2025 as foreign Developed Market (DM) stocks outperformed with a 4.7% gain to cap off a 31.6% return in 2025. DM countries have thus far emerged as the winners of the Trump tariffs, securing trade negotiation wins or circumventing the tariffs through supply chain rerouting. While the tariffs have driven US inflation to near 3%, countries such as France and Italy have seen their inflation decline as low as 1.5%. Arguably the biggest driver of DM outperformance has been US dollar weakness, which has accelerated as the Republican-controlled Congress shunned austerity in favor of record-setting levels of government spending.

Japanese stocks outperformed with a 11.3% gain in the Nikkei 225 for Q4 as new Prime Minister Sanae Takaichi advocated for pro-growth reforms over budget balancing. Takaichi’s initiatives are intended to stimulate investment in high growth areas such as AI, semiconductors, quantum computing, and biotechnology, while also lowering the cost of living for Japanese citizens. Thus far, investors have cheered the change in direction, propelling the Nikkei to a 29.0% total return during the year.

Emerging Market (EM) stocks also outperformed US stocks in 2025, with a solid 4% fourth quarter return. While a weaker US dollar contributed heavily to the EM gains, exposure to the growing AI industry was also a major driver with many AI supply chain companies domiciled in EM countries such as China, South Korea, and Taiwan. China has been the main trade adversary of the Trump administration and has shown a willingness to exert its leverage over rare earth minerals to extract tariff exemptions. If the emergency powers argument for tariffs is struck down by the US courts, China and other EM countries would benefit, although the Trump administration has expressed a willingness to pursue other pathways towards tariffing foreign goods.

Fixed income asset classes turned in a decent quarter across most asset classes, with short-duration assets and credit outperforming long-term bonds as the Fed’s rate cuts steepened the yield curve. Strong US GDP growth quelled recession fears and led to narrower credit spreads for US investment grade and high yield corporate bonds. US high yield bonds tacked on 1.4% for the quarter to cap off a solid 8.5% total return for the year. Emerging market local currency bonds were major outperformers as the US dollar weakened, gaining 3.4% during the quarter.

The Fed has been under political pressure to cut rates under the assumption that doing so will make mortgages and auto loans more affordable, but the long end of the yield curve ended slightly higher than where it began. Investors are demanding higher term premium to take on the risk of holding bonds while the government

spends recklessly, and the Fed’s control over the long end of the yield curve appears likely to remain minimal if the budgetary disfunction continues.

CLOSING REMARKS

The first quarter served as a stark reminder that geopolitical risk can appear suddenly and reshape an investment landscape that appeared broadly constructive just weeks earlier. The sudden outbreak of military conflict in Iran introduced an energy shock that markets are still trying to fully price, layering onto an existing set of challenges that include sticky inflation, a softening labor market, and a Federal Reserve that has little room to maneuver in either direction. The near-term path for equities will be heavily influenced by developments in the Middle East, and specifically whether a negotiated resolution to the Strait of Hormuz disruption can be reached before energy prices work their way more aggressively through the inflation data.

Despite the headwinds, there are meaningful reasons for measured optimism over the remainder of 2026. S&P 500 earnings growth is tracking at a double-digit rate, corporate balance sheets remain healthy, and the valuation reset in equity markets has made stocks relatively more attractive now versus earlier this year. The structural rotation towards value and small cap stocks and away from mega-cap concentration presents a healthier and more durable form of market participation. While prior experience does not dictate future performance, years that begin with a negative first quarter can still produce full-year gains, and the underlying power of the US economy provides hope that a US recession can be avoided.

Investors cannot rule out a sudden cessation of hostilities as President Trump grapples with the pressure of falling approval ratings and rising gas prices. As the November 2026 midterm elections grow closer, calls to end the conflict will grow louder, and President Trump has already attempted to declare victory in statements akin to President George W. Bush’s famous “Mission Accomplished” celebration during the Iraq war. All things considered, markets have held up well during the onset of the war, attributable to investors’ expectations that Trump will eventually tire of the ordeal. The war could end as quickly as it began, which would trigger a violent move upward that investors must be prepared for. Until then, we can only hope for a speedy resolution and the safety of all US service members everywhere.