WEEKLY MARKET SUMMARY

Global Equities: Good economic data and a solid start to earnings season combined to keep stocks positive during the week. The S&P 500 ended the weekly session up 0.6% and the Nasdaq Composite rose 1.5% thanks to continued strength in the technology sector. The more defensive Dow Jones Industrial Average lagged with a weekly decline of -0.1%. US Small Caps slipped on Friday but still managed to salvage a positive weekly return of 0.3%. Foreign Developed Market stocks were relative underperformers, closing out the week down -0.7%, while Emerging Market stocks gained 1.7%.

Fixed Income: Bond markets were jittery as continued political pressure on Fed Chair Jerome Powell triggered concerns that the Fed will lose its credibility as an independent entity. 10-Year US Treasury yields rose to nearly 4.5% before easing slightly to end the week at 4.43%. High yield bonds finished 0.2% higher during the week. It has been a record year for trading activity, with JP Morgan noting this year’s average daily trading volume of high yield bonds is up 14%.

Commodities: Crude prices eased slightly, with US West Texas Intermediate ending the week at $67.34. US drillers added oil and gas rigs to production for the first time in 12 weeks, increasing the Baker Hughes Rig count by seven. Gold prices were lower during the week, slipping to $3,356/oz.

WEEKLY ECONOMIC SUMMARY

Inflation Data: New data on Consumer prices (CPI) and Producer prices (PPI) was released mid-week, showing some continued progress but not enough to push the Fed towards a July rate cut. CPI was up 0.3% for the month as expected but prior month revisions pushed the annual rate higher to 2.7%. Core (ex-food and energy) CPI was lighter than estimates at 0.2% for the month and in line with estimates at 2.9% annually. PPI was flat for June on both headline and core measurements, but prior data was revised up from 0.1% to 0.3%. Demand for some services, notably travel-related industries, has slowed while prices of goods are accelerating due to tariffs. The Fed anticipates tariff-driven inflation to peak around November or December.

Powell Fired? The week kicked off with reports that President Trump had drafted a letter calling for the dismissal of Fed Chair Jerome Powell and had shown it to a handful of lawmakers. Trump later denied that he is pursuing firing Powell, saying it was “highly unlikely, unless he has to leave for fraud.” Trump could still be pursuing Powell’s early removal as Office of Management and Budget Director Russell Vought has raised alarms over the Fed’s $700 million cost overrun on a renovation of its headquarters.

Strong Start for Earnings: Major US banks kicked off earnings season with mostly strong results, although market reaction was somewhat tepid in most cases. Citi (C) had the best weekly performance of the major US banks, rising 7.3% in weekly trading. The most anticipated name of the week was Netflix (NFLX), which beat expectations but slipped on warning of lower margins in the second half. Taiwan Semiconductor (TSM) also reported, rising over 3% after announcing a 61% surge in profit on a 38% revenue increase. TSM’s results are a good sign for upcoming tech earnings as the AI trade remains in play.

CHART OF THE WEEK

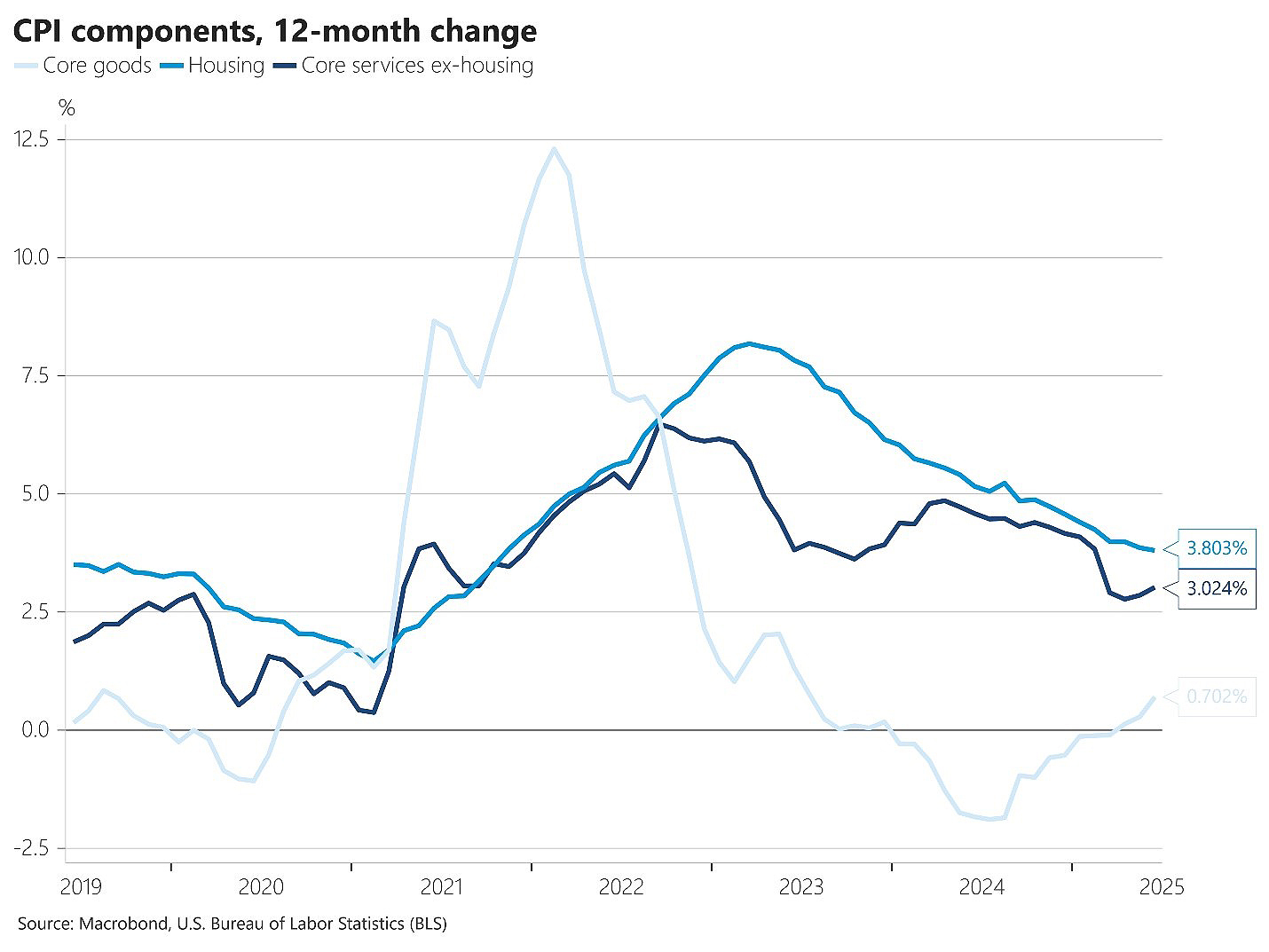

The Chart of the Week shows the annual change in CPI subcomponents, highlighting the continued challenges facing the Fed in bringing inflation down to 2%. The good news is that Housing, the most persistently sticky category, remains on the downtrend. That progress is getting partially cancelled out, however, by rising goods inflation. Services inflation had also been declining but has reversed course and is now also driving overall inflation higher. Most Fed members have voiced concerns over rising tariff-driven inflation in the coming months, making a July rate hike extremely unlikely and dropping the September odds to around 60%.