EXECUTIVE SUMMARY

2025 began with markets feeling optimistic about the incoming Trump administration’s stated goals of lower taxes and decreased federal spending. That enthusiasm was replaced with uncertainty and anxiety due to President Trump’s approach to trade negotiations, causing forecasting headaches for economists, business leaders, and market forecasters alike. Meanwhile, any hope for a leaner, more efficient Federal government has faded as the “Big Beautiful Bill” is expected to increase the national debt by $3.3 trillion over the next decade, according to the Congressional Budget Office. Despite these challenges, investors have propelled US stocks to all time highs at the mid-year mark, reflecting the continued dominance and resilience of the United States’ economy that keeps surprising to the upside.

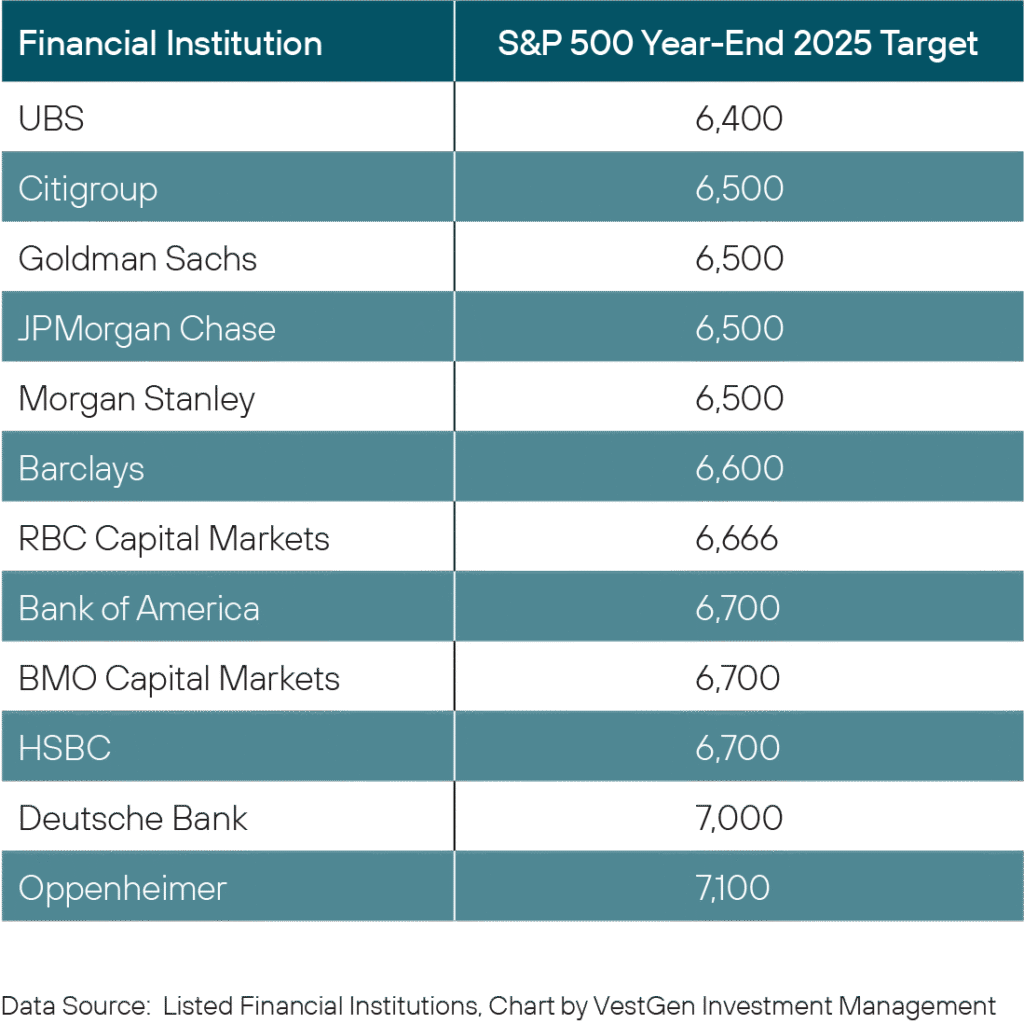

With the S&P 500 ending the first half at just under 6,200, we are still below the year-end targets that the big Wall Street banks set at the beginning of the year. These forecasts have since been revised, but looking at the original targets provides context and shows how we have outperformed given the tumultuous headlines on trade, immigration, DOGE job cuts, and now, the various geopolitical hot spots.

Despite the strong first half results, there are some warning signs. The bond market is showing signs of discontent with Federal spending. Borrowers at the long end of the yield curve are becoming less inclined to lend to the US government without higher rates due to the ballooning US federal deficit. Inflation also may be awakening from a first half slumber, with measures of Goods inflation flipping from negative to positive while Services and Housing continue to run hot.

Figure 1. Wall Street Massively UnderExhibit 1. 2025 S&P 500 Year-End Price Targets (From January 2025, prior to any revisions)estimated 2024 Performance

ECONOMIC BACKDROP

While it was known that President Trump would seek to rectify trade imbalances, the market was unprepared for the severity of the April 2nd “Liberation Day” unveiling of tariffs on nearly every US trading partner. The tariffs were derived from each country’s trade imbalance with the US and were far higher than nearly anyone expected, ranging from 11% to 49%. The unexpectedly aggressive approach sent stocks into correction territory under the assumption that the tariffs would make global recession unavoidable. The panic was short-lived, however, as President Trump issued a 90-day pause just seven days later after various business leaders warned that the tariffs would cause inflation and recession. Trump instead opted for a 10% across-the-board baseline tariff while the administration targeted a goal of “90 deals in 90 days.” China was notably excluded from the pause for retaliating, which commenced a tit-for-tat period of escalation that saw US-China tariffs reaching an almost comical level of 125%, with threats to go higher, effectively eliminating all trade between the two countries.

Cooler heads prevailed in early May with the US and China agreeing to tariffs of 10%. Since then, investors and economists have struggled to get a handle on a whirlwind of on-again, off-again trade war announcements, leaks, and rumors, with the added complexity of the US Court of International Trade (CIT) declaring the tariffs unlawful. The CIT ruling was, of course, appealed by the Trump administration and the tariffs remain in effect while the case works its way through the court system and most likely to the Supreme Court.

The US joined Israel in military action against Iran, which resulted in tariffs to fade a bit as the main driver of markets, but the cessation of the 90-day pause loomed on July 9th, causing many to wonder what’s next. To date, the administration has only signed very few trade deals, falling far short of the targeted 90 deals. President Trump has dismissed the significance of the July 9th deadline, stating he will simply send letters to each trading partner informing them of their new effective tariff rates.

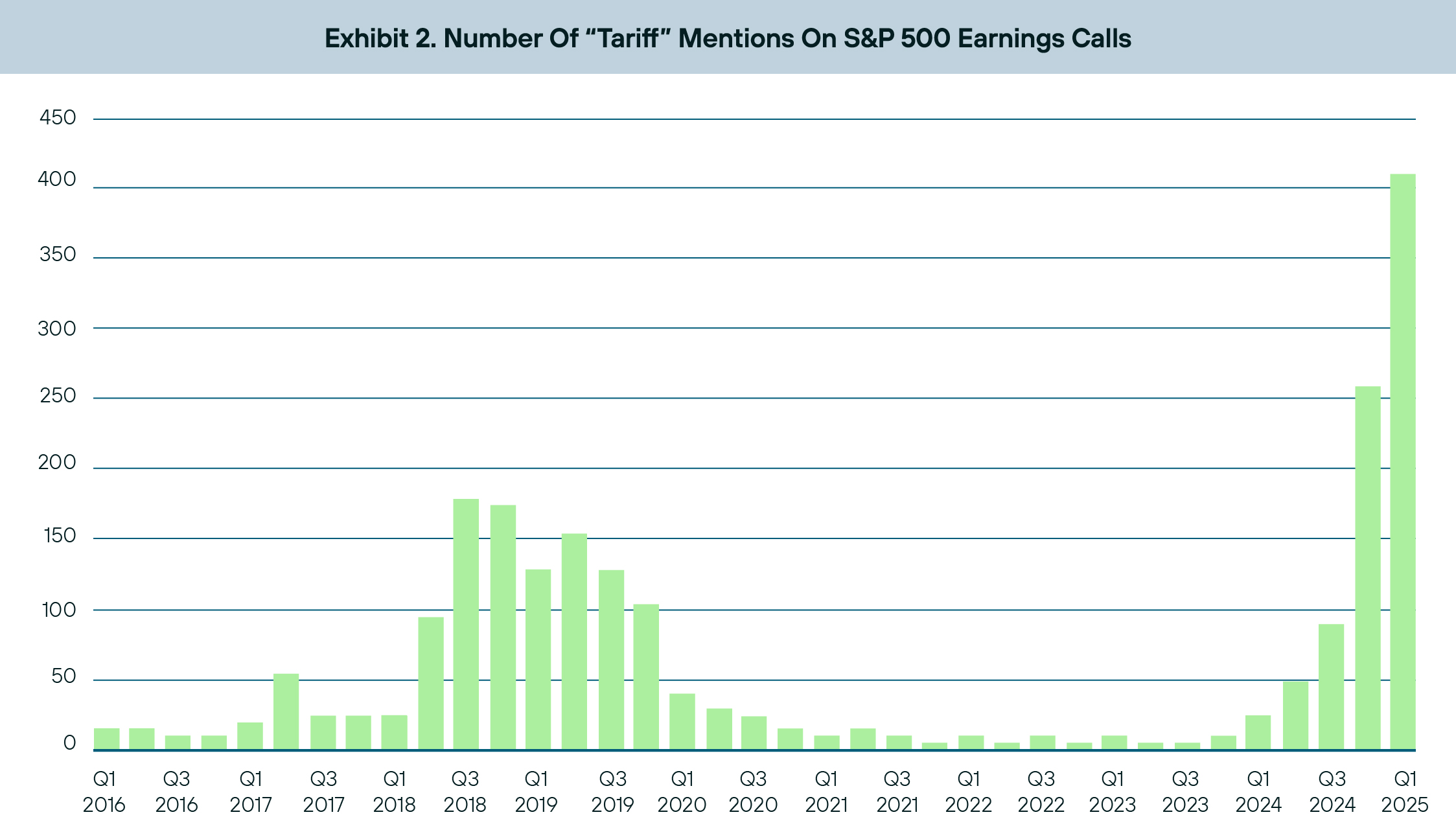

The effects of the tariffs extend far beyond the simple monetary charges being placed on goods. While not ideal, businesses and economists can adapt to tariffs. The problem with these tariffs has been the completely unpredictable and constantly changing nature of the announcements. 91% of S&P 500 companies cited tariff uncertainty in first-quarter earnings calls, with some companies withdrawing earnings guidance due to the unknown and rapidly shifting nature of the tariff war.

The US Federal Reserve (“the Fed”) has been similarly paralyzed by tariff uncertainty. At the start of the year, it was widely anticipated that the Fed would take a first-quarter breather on rate cuts to assess the impact of President Trump’s trade policy. Now halfway through the year, the Fed has not gained enough clarity to resume rate cuts. During recent Congressional testimony, Chairman Jerome Powell suggested that, absent the tariffs, the Fed would have already cut rates. As it stands, the Fed is hesitant to cut with most economists agreeing that the net effect of tariffs is higher domestic inflation and reduced economic output, the dreaded “stagflation” scenario that the Fed has less power to combat.

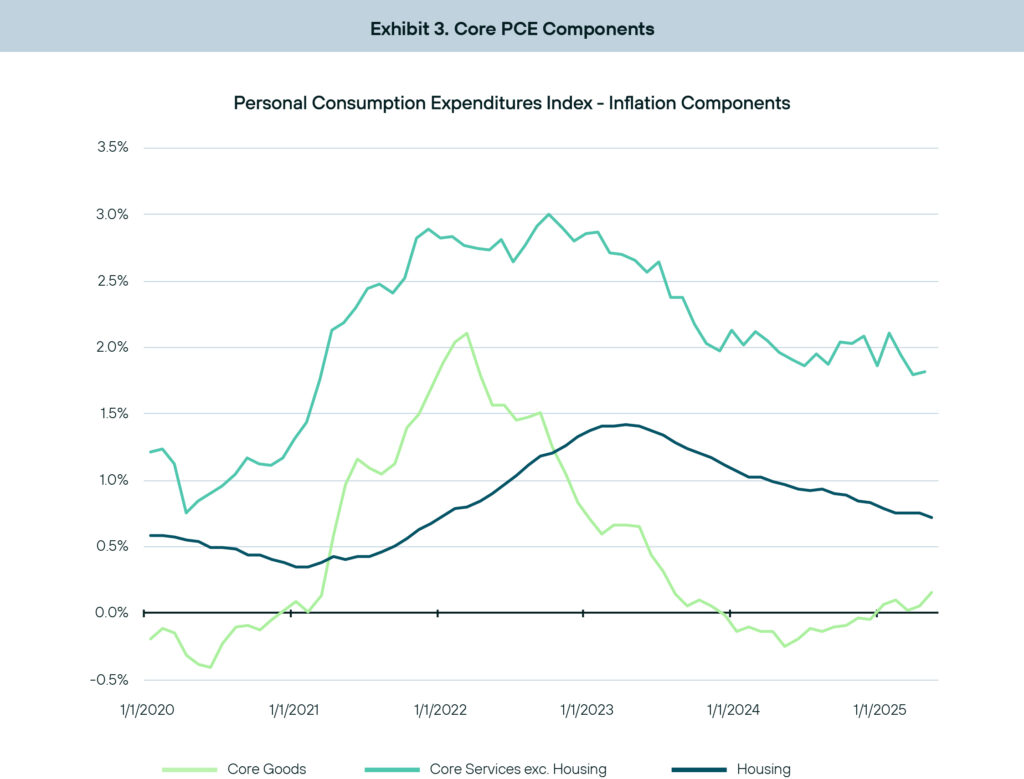

Powell also noted the Fed is placing more weight on forward-looking inflation projections than the trailing inflation data, which has been relatively benign at an annual rate of 2.7% (using the Fed’s official measure of the Core Personal Consumption Expenditures Index, or “PCE”). The Fed is projecting Core PCE will rise to 3.1% by the end of the year as tariff costs work their way through the economy. While the fears of widespread tariff-driven price inflation have not come to fruition, there are some underlying indicators that suggest the Fed is right to be cautious about inflation slowly creeping into the data. Analysis of the Core PCE component data shows that Core Goods, which were in deflationary territory, are now showing accelerating inflation, negating gradual progress in the Housing and Core Services sectors.

Even with the anticipated uptick in inflation, the Fed has been quick to point out that the US economy is otherwise on very strong footing with solid wage growth, low unemployment, and healthy consumer spending that should keep the US out of a recession despite a diminished 2025 GDP growth rate forecast of 1.4%.

US EQUITY

Normally, equity investors would be feeling confident with stocks hitting all-time highs; but 2025 has been clouded by extreme uncertainty due to the tariff situation, with additional headwinds of geopolitical strife and a higher equity risk premium as lawmakers pile on debt. The counterweight to these worries is the Artificial Intelligence (AI) revolution, which continues to drive US stock market dominance and still appears to be in the early stages of growth. US stocks have been proven winners for multiple years and investors have no reason to doubt their resilience. Still, with such a strong rally already booked in the first half, will investors get exhausted from political unpredictability?

The April 2nd “Liberation Day” tariff reveal was a gut-punch for equity investors, but the V-shaped recovery was swift and the S&P 500 closed out the first half at all-time highs. Stock investors have grown somewhat accustomed to the tariff chaos in what has become known as the “TACO” trade, short for “Trump Always Chickens Out”. Traders are now treating most of Trump’s aggressive negotiating tactics as empty threats, wagering he will be unwilling to sacrifice stock market performance in exchange for “winning” the trade war.

While ignoring Trump’s tariff bluster and staying invested has thus far been a winning strategy, the administration’s lack of progress in securing trade deals thus far warrants some caution. In our 2025 outlook, the best-case scenario presented was that Trump could quickly extract some easy “wins” from trading partners and ease off the isolationist rhetoric. This scenario did not play out, and it appears most trading partners are calling Trump’s bluff and waiting him out. As the tariff negotiations drag on, the impact on the economy will become more substantial, since tariffs are a “tax increase” on US businesses and consumers and detrimental to GDP growth and business investment.

The good news is that capital expenditures remain strong from high-growth businesses with AI at the forefront. While Technology Sector stocks (represented by the SPDR Technology Sector ETF XLK) lagged the broader S&P 500 index by -7.5% from January 1, 2025 to the April 8th low, they outperformed the S&P 500 on the rebound by 16.9% as the tariff pause coincided with stellar earnings results in the first quarter. This AI-driven strength shows no indication of fading, either. Technology sector earnings are projected by FactSet to grow at nearly 17% in the second quarter, driven by an anticipated 33% earnings per share (EPS) growth rate for Semiconductor industry stocks. Communication Sector stocks, with AI names like Alphabet (GOOG) and Meta (META) are also poised to continue their leadership role in Q2. Nvidia (NVDA), the leading AI related company in the world, hit a $4 trillion dollar market cap, the first company worldwide in history to achieve that valuation.

For the S&P 500 in aggregate, earnings are anticipated to grow at an annual rate of 5.0% in the second quarter, which is a significant downgrade from the 9.4% EPS growth projected just prior to the “Liberation Day” announcement. Energy and Consumer Discretionary stocks will likely begin to show signs of strain, with geopolitical events being a drag on the former and tariffs significantly impacting the latter. Forecasting full year growth is tricky with the volatility of tariffs remaining a wildcard, but consensus estimates presently call for EPS growth of 9.1%, down only slightly from 2024.

With AI-related, high growth stocks resuming the leadership position, investors now must question whether stocks are priced “for perfection” and how much upside remains. The S&P 500 and Nasdaq Composite indices are sitting at technical levels that can be considered “overbought”, with the S&P 500 and Nasdaq both registering a Relative Strength Index (RSI) reading at 72 as of June 30, 2025. An RSI below 30 is considered oversold and a reading above 70 is overbought. Strong quarterly earnings will have to be delivered and, perhaps more importantly, CEOs will have to bring an upbeat tone to the earnings calls if the rally is expected to continue. In the second half of 2025, investors should also consider rebalancing into stocks with defense and infrastructure exposure, which should benefit from the substantial pork in the “Big Beautiful Bill” which includes a whopping $1 trillion allocation to Defense spending.

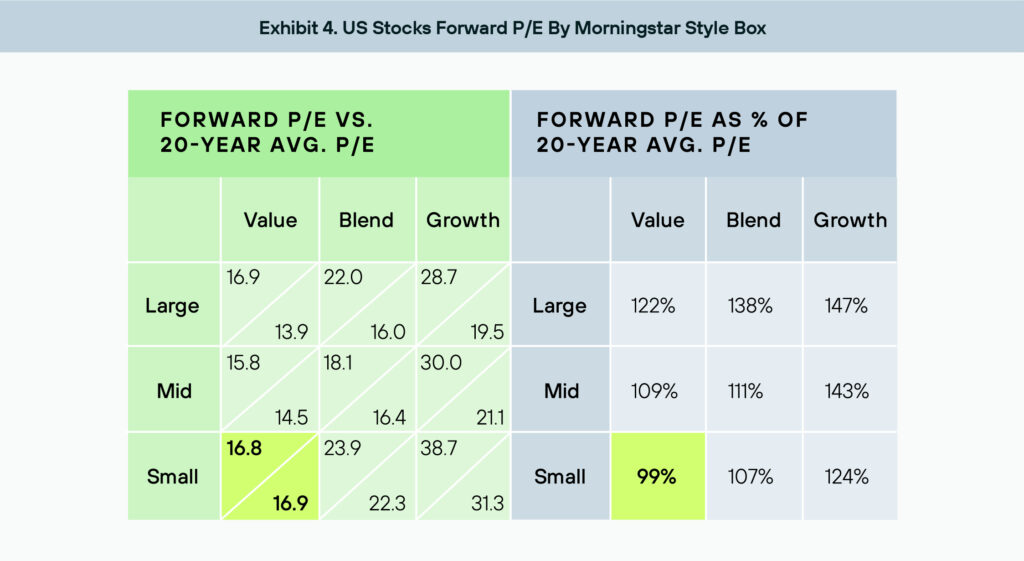

US investors have tried to allocate to cheaper, unloved Small-Cap and Mid-Cap (“SMID”) stocks in the first half of 2025, despite the challenges that tariffs bring to smaller firms with less pricing power. SMID stocks have rallied off the April 8th lows yet remain historically cheap relative to Large Caps. Small Caps are trading at a 17% discount on their Morningstar fair value estimate at quarter end and should eventually benefit from tariff-driven reshoring and Fed rate cuts later in the year. Small Value stocks are trading at a 16.8x forward price-to-earnings (P/E) multiple and are the only one of the nine Morningstar “style boxes” presently at a discount (albeit a slight one) to their 20-year average P/E ratio.

We would be remiss not to point out that, amidst all the uncertainty, is the possibility that Trump simply tires of his tariff campaign, declares victory, and settles for more benign, permanent tariff rates on our trading partners. The self-inflicted nature of the tariffs, and the ability of the President to instantly undo the damage if he elects to, has been the upside risk on the table since the measures were announced early in 2025. The volatility and unpredictability can be tough to stomach, but there are plenty of reasons to stay heavily invested in US stocks in the second half.

DEVELOPED INTERNATIONAL EQUITY

Global diversification finally paid off in the first half of 2025 with foreign stocks shrugging off tariff threats and demonstrating rare outperformance over US equities. European stocks crushed their US peers with the STOXX Europe 50 Index gaining 24.4%, beating the S&P 500 by over 18% in the first half of the year. A major driver of the Eurozone strength was the European Central Bank (ECB), which cut its key interest rates multiple times while the US Federal Reserve elected to hold rates steady.

The weaker US dollar also attracted flows to European equities, which have become an increasingly smaller portion of global portfolios after years of US dominance. For investors who have seen their US-domiciled Technology sector stock exposure grow substantially in recent years, a rotation into European stocks which are dominated by Financials and Industrials provided a rebalancing opportunity at attractive earnings multiples. Eurozone stocks began the year at just a 12.9x forward P/E multiple, which has risen to a still attractive 14.3x following the first half gains.

Outside the Eurozone, Japan is the other major developed market of note, representing roughly one-fifth of the MSCI EAFE Index, the developed market benchmark which excludes the US and Canada. Japanese stocks faced significant headwinds from tariffs, which impacted the automotive industry and other exports to the US. Corporate reforms were able to offset some of these challenges, but volatility in the Yen was a drag on exporters as it ultimately sharply appreciated against the US dollar. If the US dollar can bounce back from its 7.9% first half devaluation vs the Yen, Japanese equities could be a source of outperformance for Developed International stocks in the second half. Japanese equities are currently also priced at a discount to their US peers at 14.8x forward earnings.

Tariffs are a concern for Developed International stocks, but not as much as one might think. Companies represented in the MSCI EAFE Index derive 21% of their revenues from North America (with the vast majority being the US). Some of the larger, foreign multinationals have shown a willingness to “play ball” with President Trump and move manufacturing to the US, most notably in the automotive, pharmaceutical, and semiconductor industries. Yet with the unstable and constantly shifting tariff developments, many foreign companies are simply waiting for clarity before incurring the costs associated with relocating their operations.

The US still dominates in high growth technology industries, particularly in AI, but Developed International stock exposure proved its worth in the first half and remains a foundational component for diversified portfolios. Aggregate GDP growth for the MSCI EAFE region will likely be slightly below that of the US in 2025, with a consensus estimate of 0.9%. Investors who have not recently rebalanced, or who have avoided the Foreign Developed asset class completely due to years of underperformance, should take note and consider that EAFE has at least some representation in their portfolios.

EMERGING MARKETS

Emerging Market (EM) stocks also outperformed as investors rotated out of US stocks over concerns surrounding valuations and domestic economic policies. The weaker US dollar was a major driver for investment in Emerging Markets, as were attractive valuations with EM stocks that began the year at just a 12.0x P/E multiple, which has risen slightly to 12.9x as of June 30th, 2025. Emerging Market stocks were able to gain 15.3% in the first half despite massive uncertainty over US trade policies.

Despite China drawing most of President Trump’s ire and incurring the harshest tariffs (before they were rolled back), Chinese equities trounced US stocks, returning over 18% in the first half. Some of the outperformance was attributable to front-running of tariffs as US importers rushed to bring goods into the country during Q1 before the “Liberation Day” announcement in April. The tariffs bring uncertainty, but any investor with exposure to Chinese stocks should be well accustomed to uncertainty by now, given the Xi regime’s history of unpredictable regulations on foreign investment in China’s equity markets.

In the recent past, the Chinese government’s intervention into equity markets have caused some investors to deem Chinese stocks “un-investable” but some aspects of China’s isolationist stance may be softening. Throughout the tariff dispute and negotiations, it has become increasingly apparent that the US and China need each other to continue advances in Artificial Intelligence, quantum computing, and other high-tech pursuits. China dominates the global production of rare earth minerals, crucial for the manufacture of semiconductors and other computer components. Meanwhile, the US is the global leader in semiconductor design and manufacturing, and China is desperate to obtain the high-end chips needed for advanced computer applications. The relationship is complex, with national security concerns influencing trade policies, but there is no doubt that the two countries need to work together in some way to continue advancing these technologies. This gives us some optimism that cooler heads will prevail in what has been, thus far, contentious trade talks.

FIXED INCOME

The Federal Debt burden, set to increase dramatically with the passage of the “Big Beautiful Bill”, was top of mind for fixed income investors during the first half of 2025. Bond investors expressed this concern by demanding higher rates, particularly on the long end of the Treasury curve, which saw 30-Year Treasury yields rising as high as 5.1% during May. Other indicators of bond market volatility raised alarms such as the MOVE index, which spiked to 140 after the tariffs were announced. For comparison, the MOVE index typically sits around 87 and reached 160 during the pandemic. The message of the bond market ultimately fell on deaf ears in Congress, which could spell trouble for long US Treasury bonds as foreign investors appear to be rethinking their willingness to lend to the United States.

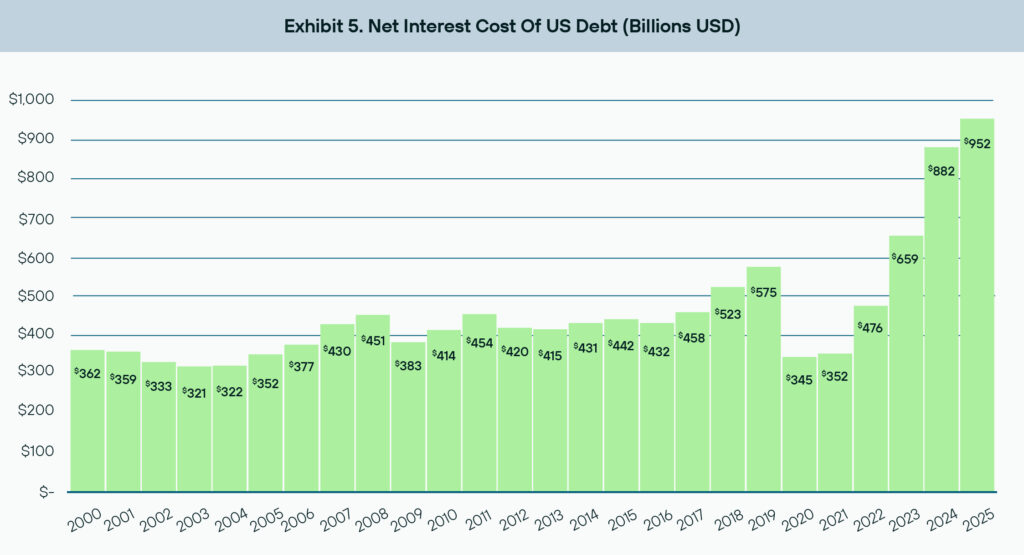

The US Treasury will be borrowing trillions of dollars more than before under the “Big Beautiful Bill”, which raised the debt ceiling by $5 trillion. Significant tax cuts in the bill will also decrease federal tax revenue and worsen the deficit. The Trump administration maintains tariffs will make up the difference, but most economists doubt that proposition. Any savings from Elon Musk’s DOGE initiative are a drop in the bucket compared to the spending increase Congress is poised to unleash, with some independent sources suggesting DOGE cost taxpayers far more than it ultimately saved. While the Fed’s decision to keep interest rates elevated affords them some “dry powder” in the event of a recession, it is also costing US taxpayers nearly a trillion dollars in annual interest payments on the ever-growing Federal debt.

With massive volume of new issuance on the horizon to satisfy Congress’ spending addiction, there will likely be upward pressure on the long end of the yield curve, which could steepen even further. Lawmakers have attempted to make up for waning foreign demand by relaxing regulations and in some cases promoting “stablecoins” which are dollar-pegged cryptocurrency instruments that are supposedly backed by one-to-one Treasury reserves. Yet, this approach introduces new risks to the Treasury markets and will likely only alleviate the need for buyers at the short end of the curve, leaving the lack of long-term Treasury demand a remaining issue.

Congress’ unsustainable spending comes at a hefty cost in the form of higher interest with the Fed holding its benchmark lending rate at 4.25-4.5% until at least September. The net effect of all the spending is that US long-term bonds may no longer provide the downside risk protection they had in the past. Fixed income investors who remained in short-term bonds fared much better, with 3-Month US Treasury Bills yielding 4.3% or better for nearly all of 2025 YTD, with significantly lower volatility.

Despite concerns that tariffs could trigger slower growth or even a recession, corporate bonds bounced back sharply from the April lows and surged in the second quarter. Corporate debt across the entire risk spectrum saw heavy demand, compressing spreads to near two-decade lows for both investment grade and high yield bonds prior to the tariff announcement. Overall US corporate bond issuance is at $1.17 trillion already, a 5.2% year-over-year increase, and indicates a healthy market and willingness for firms to engage in capital expenditures. There is some corporate debt rollover risk as debt comes due in the coming years, with $642 billion maturing in the second half of 2025, $930 billion in 2026, and $860 billion in 2027. Much of this debt was originally borrowed at lower rates and will need to be refinanced.

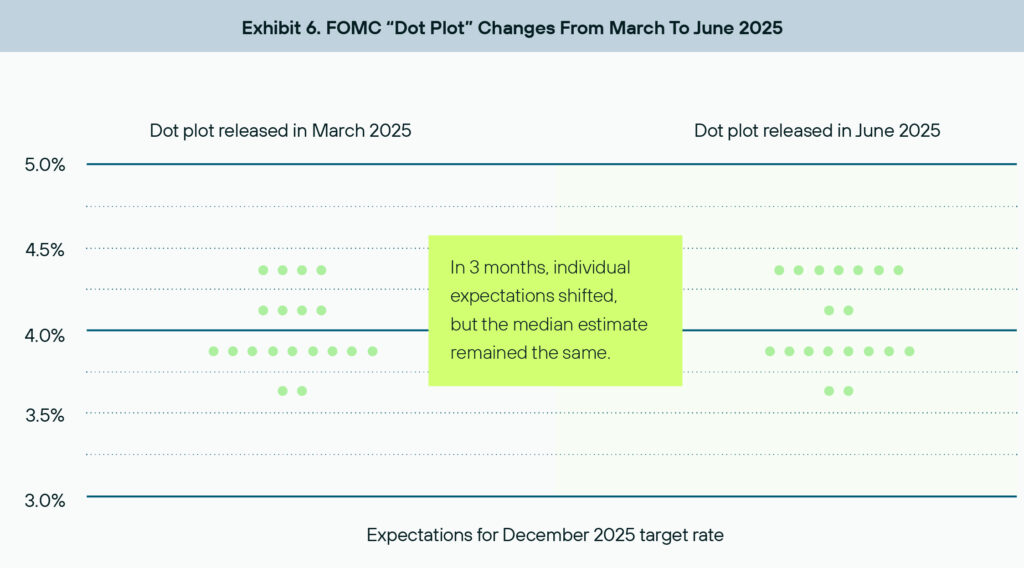

Fixed income investors need to tread carefully in the second half, closely monitoring inflation as there is a chance the Fed elects to not cut rates in September or even at all in 2025. Despite no change to the median forecast, the underlying votes from the Fed show some members have shifted more hawkish in recent meetings (hawkish means less likely to reduce rates, dovish means less likely to increase rates). Seven FOMC members were in the “no 2025 rate cut” camp at June’s meeting compared to four in March, as shown in the June FOMC “Dot Plot” summary of interest rate projections.

Markets are always forward-looking and rate cuts in 2026 are inevitable regardless of the inflation data. Fed Chair Jerome

Powell is virtually guaranteed to be replaced with a new Chair of Trump’s choosing, who will almost certainly be an advocate for rate cuts, and possibly aggressively. While markets would typically cheer the ensuing rate cuts, there is also reputation risk of a politicized Fed losing its status as an independent entity if/when Powell is replaced next year.

COMMODITIES AND ALTERNATIVES

While a key part of President Trump’s campaign promise was to unleash US energy production and “drill baby drill”, the truth is that US oil producers were already pulling more crude out of the ground than the market can handle, even with OPEC trying to limit the supply of oil in the market via production cuts. US West Texas Intermediate (WTI) crude prices slipped through the first quarter as demand could not meet supply, bottoming out around $55 a barrel in May. The Israel-Iran conflict triggered a brief surge above $75, but since then prices have settled in around the $65-$70 range.

Despite a lifting of regulations, US drillers have continuously decreased the active rig count, which has fallen to its lowest level post-pandemic. The rationale is a mix of greater efficiency in extracting oil and caution from drillers worried about waning demand. Many oil companies are electing to spend profits on buybacks and dividends rather than expanding output. President Trump has attempted to juice the industry via budget bill provisions designed to both reward oil production and make green energy options much less attractive by removing tax credits, but ultimately, global growth expectations will determine the path of crude prices in the second half.

Precious metals were a big winner in the first half, with gold prices surging 24% in the first half to an all-time high above $3,500. Gold eased a bit to end the first half at around $3,300 but should continue to find buyers looking for diversification and protection from inflation and the declining US dollar. Other precious metals such as platinum (up 54%) and silver (up 25%) saw similar gains in the first half. Industrial metals such as copper, aluminum, and steel have also performed well in the first half of the year due to tariffs and other trade restrictions, despite a pullback in forecasts for global growth.

Investors hoping that Real Estate would finally bounce back were disappointed in the first half of the year, as high rates kept the lid on any rallies. The Dow Jones Equity REIT Total Return Index was essentially flat in the first half, up just 0.7%. REITs are a diverse group, however, and as was the case in prior years, performance was differentiated among the sub-industries within the sector. Defensive healthcare REITs were relative outperformers thanks to aging demographics and several high-profile mergers. Data center REITs were also frequently in the headlines as the engine driving the AI revolution. Residential REIT performance was lackluster, despite high interest rates keeping renters priced out of the housing market, which helped maintain occupancy rates. Office REITs remain challenged and will continue to see limited demand with remote and hybrid work remaining an increasingly permanent part of the

US economy.

FINAL THOUGHTS

Investors had to recalibrate expectations for 2025 after the tariff announcement altered the outlook for stock returns and rate cuts. The uncertainty has not fully dissipated, but the market’s V-shaped recovery off the April low and on to new all-time highs once again demonstrated the benefits of remaining calm and staying invested in times of turmoil. Diversification also made a welcome comeback after years of lopsided US dominance, with international stocks finally outperforming their US peers. As we look ahead to the second half, tariffs remain in the spotlight with the threat of escalation always a possibility. The fact that President Trump paused tariffs after the initial market shock leads us to believe he will not risk sacrificing stock market performance for tariff concessions, so there is hope that we finally settle on less punitive rates in the absence of actual signed trade deals.

Some tariff-driven inflation will be unavoidable, however,

and the Fed has become more hawkish in recent meetings as more FOMC members shift to the “no rate cut” camp for 2025 as shown in the June “Dot Plot” summary of interest rate projections. Stocks have already shrugged off the disappointment of delayed rate cuts multiple times, however, so if AI and other growth industries can keep delivering on their promises and deliver Q2 earnings beats, the US stock market is set up to take another leg higher. The margin for error has certainly tightened but we remain optimistic that there remains further upside for what has been a remarkably resilient market, both in the US and abroad.

Thank you, as always, for the opportunity to let us serve you.

Commentary by VestGen Investment Management. VestGen Investment Management is an SEC registered investment adviser with its principal place of business in the State of New Jersey with offices at 3393 Bargaintown Rd., Egg Harbor Township, NJ 08234. Being a registered investment advisor does not imply any level of skill or training. VestGen Investment Management and its representatives are in compliance with the current registration and notice filing requirement imposed upon registered investment advisers by those states in which VestGen Investment Management maintains clients. VestGen Investment Management may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements. This weekly update is limited to the dissemination of general information. Any subsequent, direct communication by VestGen Investment Management with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status, service and fees of VestGen Investment Management, please contact VestGen Investment Management or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about VestGen Investment Management, including fees and services, send for our disclosure statement as set forth on Form ADV from VestGen Investment Management using the contact information herein. Please read the disclosure statement carefully before you invest or send money.