WEEKLY MARKET SUMMARY

Global Equities: The Iran conflict entered its fourth week with no resolution in sight, dragging stocks to a fourth consecutive weekly decline. Uncertainty over the flow of global oil through the Strait of Hormuz was the primary driver of market volatility, which was exacerbated by hotter than anticipated inflation data. The S&P 500 finished the weekly session at a four-month low, declining -1.9%. The Nasdaq Composite slid -2.1% while the Dow Jones Industrial Average slipped under its 200-day moving average amidst a -2.1% pullback. US small cap stocks continued to struggle under the weight of rising borrowing costs, slipping into correction territory after falling -1.6% during the week, while foreign developed market stocks fell -2.8% as Europe grappled with energy supply uncertainty. Emerging market stocks also posted steep weekly losses, ending -2.0% lower.

Fixed Income: Treasury yields rose sharply across the curve, pushing the 10-year yield up to 4.37%. Market expectations for a rate cut in the first half of 2026 have all but vanished, with Fed Funds futures markets pricing in 0% odds of a cut and 16% chance of a rate hike in the June meeting, according to CME Group’s Fedwatch tool. The odds of a September meeting cut have also fallen to zero, and a December rate cut stands at just a 6% likelihood.

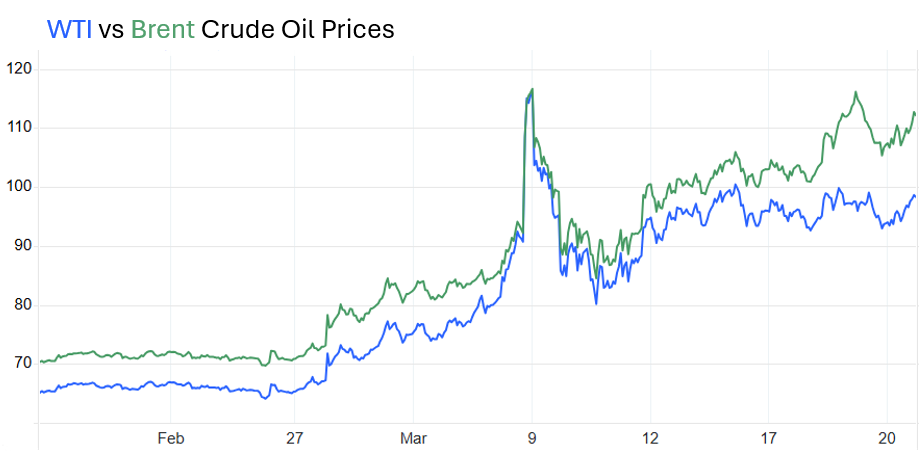

Commodities: Oil prices remained under pressure, although US benchmark West Texas Intermediate prices were relatively more stable than their international counterpart, Brent Crude. WTI prices ended the week slightly higher at $98.40 a barrel, while Brent prices closed out the session at $106 after spiking to nearly $120 midweek. Iran’s new Supreme Leader, Mojtaba Khamenei, has said the Strait of Hormuz should remain closed as a “tool to pressure the enemy,” while President Trump attempted to convince allies to assist in securing safe passage for ships traveling through the strait. Gold, which had served as a safe haven earlier in the crisis, came under pressure as rate hike expectations crept into the market, falling over -9% during the week to $4,570/oz.

WEEKLY ECONOMIC SUMMARY

Hot Inflation: The Producer Price Index (PPI) unexpectedly shot up 0.7% in February, while core PPI (excluding food and energy) rose 0.5%. It was the second consecutive hot print for PPI, which rose to an annual rate of 3.4%. The data reinforced concern that inflation was already running warm before the energy shock was even fully captured in the numbers, suggesting the readings in coming months will be meaningfully worse.

Fed on Pause: The Federal Reserve kept its benchmark rate unchanged at 3.5-3.75%, as anticipated, in an 11-1 decision. The lone dissenting Fed member was Trump appointee Stephen Miran, who holds a temporary seat pending the confirmation of Kevin Warsh. At his press conference, Chair Powell said the Fed’s forecast is that progress on inflation will continue, “not as much as we had hoped, but some progress.” Powell declined to use the word “stagflation” to describe the current environment despite the Fed increasing its inflation projection from 2.5% to 2.7%.

Global Central Banks Remain Cautious: In addition to the US Federal Reserve, the European Central Bank, the Bank of Canada, the Bank of Japan, and the Bank of England all concluded their March meetings this week, each opting to leave policy rates unchanged. While the Bank of Canada and ECB struck a measured, wait-and-see tone, the Bank of England took a notably more hawkish stance, removing prior commentary around expectations for future rate cuts and emphasizing the need to return inflation to its 2% target. The Bank of Japan signaled it will likely continue raising rates if economic activity evolves in line with expectations.

CHART OF THE WEEK

The Chart of the Week shows the widening spread between West Texas Intermediate (WTI) Crude oil and Brent Crude. WTI is the domestic benchmark for oil produced in the United States while Brent is the global benchmark, representing oil produced in the North Sea. While both WTI and Brent prices moved sharply higher due to the war in Iran, the transportation bottleneck in the Strait of Hormuz has triggered a divergence in prices, pushing the spread between the two oil varieties to its widest margin since March 2013 (excluding the negative WTI prices in April 2020).

Commentary by VestGen Investment Management.