WEEKLY MARKET SUMMARY

Global Equities: Markets continued their euphoric rally, propelling the S&P 500 4.5% to a new all-time high above 7,100 as investors cast off any lingering concerns over the war in Iran. A 10-day ceasefire between Israel and Lebanon provided further rationale for optimism, pushing the Nasdaq Composite an impressive 6.8% higher to close out a 13-day winning streak at a new all-time high. The Dow Jones Industrial Average gained 3.2% but has still yet to retake the 50,000-mark crossed earlier this year. US small cap stocks also set new all-time highs as the Russell 2000 gained 5.6% during the week. Foreign developed market stocks lagged their US counterparts, gaining 2.1% during the weekly session, while Emerging Markets fared better as relief in oil prices lifted the MSCI Emerging Market Index 5.1%.

Fixed Income: Treasury yields trended lower during the week, with the 10-Year ending Friday at 4.26%. Softer-than-anticipated producer price inflation data and the prospect of a conclusion to the Iranian conflict provided dual tailwinds for fixed income. Odds of a December 2026 rate cut edged higher to just under 50%, a vast upgrade from just a few weeks ago when investors were speculating the Fed could implement rate hikes by year end.

Commodities: The announcement of a deal to reopen the Strait of Hormuz triggered a violent collapse in oil prices late in the week, with West Texas Intermediate tumbling to around $85.50/barrel and Brent ending the week at just under $92/barrel. The celebration may prove premature, as Iran has declared the strait open but the US blockade remains in effect and tankers seeking passage are being turned back by US naval forces. With the US exerting its authority over the strait, Iran renewed hostilities towards ships attempting to pass, firing on two Indian-flagged ships over the weekend despite having granted them prior clearance to pass. The risk-on rally caused gold prices to retreat slightly, closing out the week around $4,880 per ounce.

WEEKLY ECONOMIC SUMMARY

Producer Prices Better than Feared: Recent consumer price inflation data has shown an accelerating trend, which triggered concerns that wholesale prices would also be rising rapidly. The March Producer Price Index confirmed those fears with a 0.5% monthly spike to a 4.0% annual rate of inflation, but that data was far better than economists expected. Gasoline prices accounted for nearly half of the cost increases, rising 15.7% in the month. Because a subset of PPI components feed directly into the Fed’s preferred Personal Consumption Expenditures inflation gauge, the report reinforces expectations that April PCE will show a significant inflation reacceleration.

Unexpected Manufacturing Strength: Regional manufacturing surveys defied expectations this week, offering a counterintuitive bright spot amid the ongoing energy shock. The Philadelphia Fed Manufacturing Index climbed to 26.7 in April from 18.1 in March, more than double the consensus forecast of 12. New orders and shipments were bright spots in the report, while the current employment index slipped 6 points to -5.1, turning negative and suggesting firms are expanding output but pulling back on headcount. The Empire State survey told a similarly encouraging story as the reading on general business conditions rose to a five-month high, with new orders and shipments both reaching their highest levels since 2023.

Earnings Season Picks Up: Financial sector stocks were the focal point of earnings news during the week, highlighted by beats from Goldman Sachs (GS), JP Morgan (JPM), BlackRock (BLK), Morgan Stanley (MS), Bank of America (BAC), and Citi (C) as higher rates boosted net interest income. Aside from financials, the other big earnings story was an impressive beat from Taiwan Semiconductor (TSM) driven by a 58% rise in net profit. Management cited the “insatiable” demand for AI infrastructure, which drove shares of other AI companies higher in advance of their earnings.

The week ahead: Earnings season picks up this week with results from Tesla (TSLA), Intel (INTC), GE Vernova (GEV), Blackstone (BX), ServiceNow (NOW), Boeing (BA), UnitedHealth (UNH), and others. Retail sales are the highlight of a relatively light week for economic data releases.

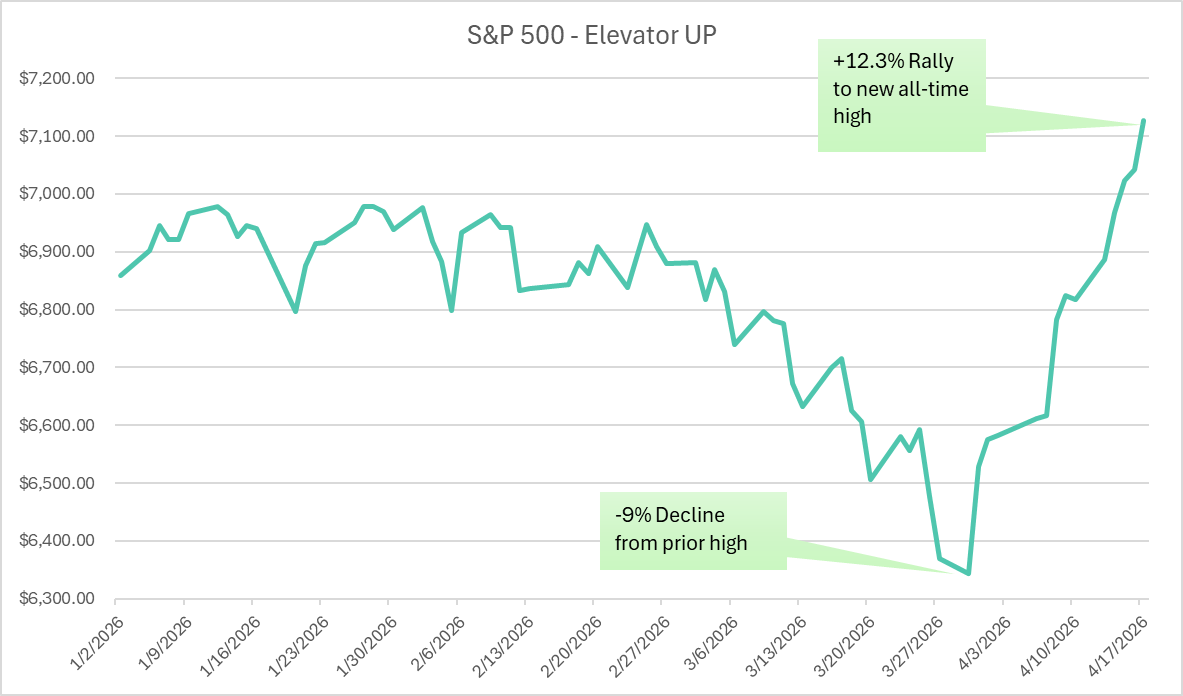

CHART OF THE WEEK

The Chart of the Week shows the year-to-date closing price of the S&P 500 Index, highlighting the rapid ascent off the March 30th low. Traditional Wall Street wisdom dictates that stocks usually “take the stairs up and elevator down”, but in this case stocks have headed straight for the penthouse suite in record time. The S&P snapped back from a -9% drawdown to a new all-time high in just 11 trading days, the fastest such recovery in 36 years according to JP Morgan, as a rapid shift in sentiment over Iran triggered substantial short covering from hedge funds needing to immediately unwind their bearish positions. The move appears to have caught many retail investors off guard, suggested by data indicating they were net sellers through the initial April bounce. With earnings now providing additional positive news and fear of missing out (FOMO) hitting smaller investors, the momentum has shifted to the side of the bulls.