WEEKLY MARKET SUMMARY

Global Equities: Stocks took a breather from their historic rally in a choppy weekly session that ended with modest gains. The S&P 500 managed a weekly gain of 0.6% as doubts over peace in Iran and concerns over AI disruption re-emerged. The Nasdaq Composite ended the week 1.5% higher thanks to a strong rally in semiconductor stocks that outweighed concerns in the software market. The Dow Jones Industrial Average lagged with a -0.4% weekly pullback, while the Russell 2000 small-cap index gained 0.4%. Vulnerability to the Mid-East energy supply chain tempered foreign developed market returns, which came in at -2.4% for the week, while emerging market stocks ended 0.2% higher.

Fixed Income: The 10-year Treasury yield climbed to 4.3% on Thursday, reaching a more than one-week high as stalled US-Iran peace efforts and continued tensions in the Strait of Hormuz kept energy prices elevated and inflation risks in focus. News that the Department of Justice was dropping its criminal investigation into Fed Chair Jerome Powell raised expectations of a 2026 rate cut to 38%, as the path is now clear for the confirmation of Trump nominee Kevin Warsh.

Commodities: The on-again, off-again negotiations news out of Iran triggered more volatility in oil markets, propelling West Texas Crude to above $97 a barrel and Brent to just under $105 as of Friday afternoon. Gold prices retreated slightly from $4,880 to $4,758 per ounce.

WEEKLY ECONOMIC SUMMARY

Retail Sales Shine: Retail sales rose 1.7% in March, well above the consensus estimate of 1.4% and the fastest monthly pace since March 2025. Gasoline station receipts surged 15.5% as higher fuel prices influenced consumer behavior, accounting for an outsized share of the headline gain. Core retail sales (excluding autos, gasoline, and building materials) also outperformed expectations at 0.7%. In aggregate, retail sales have risen 4.0% over the past twelve months in nominal terms. However, inflation-adjusted real sales are up just 0.7%, suggesting that much of the headline strength reflects higher prices rather than greater volumes.

Geopolitical Update: The week started on an optimistic note despite the cancelation of weekend peace talks. On Tuesday, President Trump backed off a Monday threat of “lots of bombs going off” as the ceasefire expired, announcing that the ceasefire would remain in place indefinitely. Iran dismissed Trump’s announcement as meaningless, and fired on three vessels in the strait, seizing two. Despite Iran’s unwillingness to open the Strait of Hormuz or come to the negotiating table, a three-week ceasefire extension between Israel and Hezbollah gave markets reason to rally. Investors were cautiously optimistic on Friday on word that Iran was sending diplomats to Pakistan to resume in-person talks.

Earnings Season: All eyes were on Tesla (TSLA) heading into the week, but it was Intel (INTC) that stole the show, gaining over 21% Friday after reporting $0.29 EPS vs $0.01 estimates. Tesla missed on revenues while better margins led to a beat on EPS, however, shares were still lower after earnings. Software stocks were under pressure once again after ServiceNow (NOW) subscription growth missed expectations, leading to a -17% decline on Thursday and triggering heavy losses across most software sector names.

The week ahead: The coming week features a packed schedule for earnings with Microsoft (MSFT), Amazon (AMZN), Meta (META), Alphabet (GOOG), and Apple (AAPL) all offering first quarter 2026 results. In addition, blue chip stocks Eli Lilly (LLY), UPS (UPS), Coca-Cola (KO), Caterpillar (CAT), Chevron (CVX) and Exxon (XOM) are also slated to report earnings during the week.

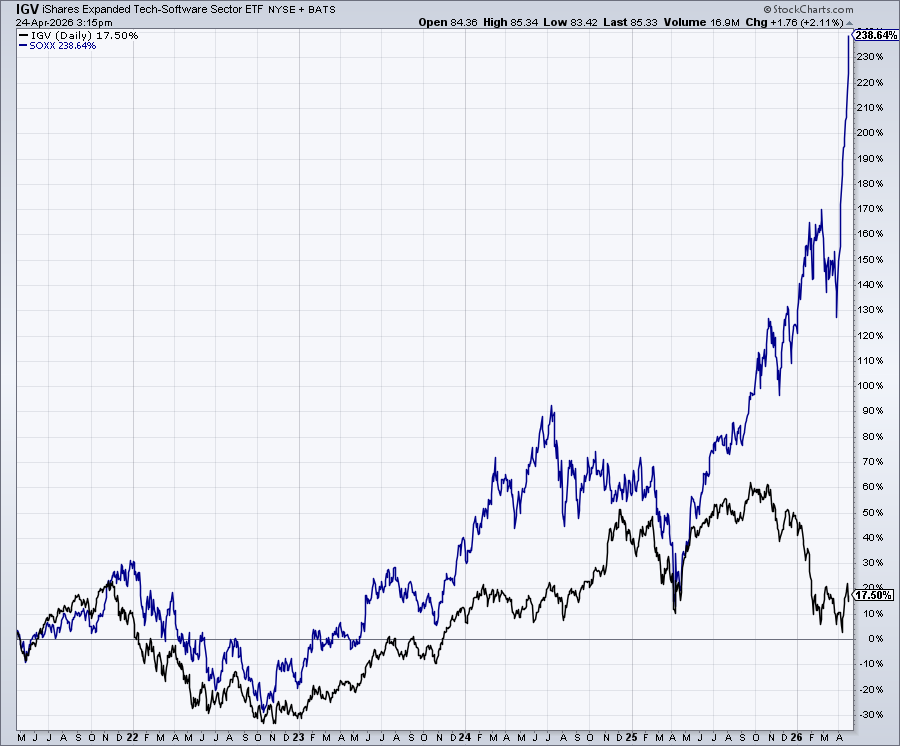

CHART OF THE WEEK

The Chart of the Week is a five-year comparison of Semiconductor stocks (blue line) and Software stocks (black line). While the two technology industries have typically moved in a highly correlated fashion, the impact of artificial intelligence has caused their paths to sharply diverge recently. Semiconductor stocks have been the primary beneficiaries of the AI trade as they struggle to keep up with insatiable demand. Software, on the other hand, faces a perceived existential threat as AI has demonstrated the ability to write computer code and potentially replace some software functionality. Essentially, the market has assigned a wider moat for hardware than software; therefore, demonstrating the ability to retain customers will be crucial for Software as a Service (SaaS) companies this earnings season.

Commentary by VestGen Investment Management.